April Update

After a bruising March, April delivered a decent reversal, a ceasefire announcement, a rekindled AI trade, and strong earnings season all converging to lift equities, even as oil stayed stubbornly elevated and diplomacy kept stumbling.

The Relief Rally: A Ceasefire Changes Everything

March left investors shell-shocked. The outbreak of direct hostilities between the US and Iran triggered a global energy supply shock, reignited inflation fears, and sent implied volatility to levels seen less than 4% of the time over the prior five years. Then, near the start of April, a two-week ceasefire was announced — and markets were relieved. In the markets view, the war is over.

The relief, however, came with significant caveats. The ceasefire ended overt fighting but did not resolve the critical question of the Strait of Hormuz, which remained effectively closed to normal shipping traffic throughout the month. Brent crude pushed above $110 per barrel by month-end, keeping energy-driven inflationary pressures firmly on the table. The IMF, in its April World Economic Outlook, revised global growth forecasts down to 3.1% for 2026, noting that risks remain "decisively on the downside."

US 10-year Treasury yields seesawed dramatically, falling to a low of 4.22% on April 17 amid fleeting reports that the Strait had reopened, before rebounding as those hopes evaporated. The net effect: yields ended the month roughly unchanged, masking a turbulent journey in between.

The Aussie Dollar: A Wild Ride to Four-Year Highs

The AUD has rallied over 20% from its April 2025 lows — but the path has been anything but smooth.

If you blinked in April, you may have missed a complete round trip in the Australian dollar. The AUD/USD has been caught in a particularly volatile crossfire: on one side, the currency is supported by an increasingly hawkish RBA, commodity strength, and a widening yield advantage over the US. On the other, every twist in the Iran ceasefire narrative has triggered sharp swings in risk sentiment, hammering a currency that remains one of the market's most reliable risk barometers.

The broader story is one of structural rehabilitation. After bottoming at just 59.22 US cents in April 2025, its lowest in five years, the AUD has staged a remarkable recovery, climbing back above 0.71 by April 2026. The drivers are well understood: the RBA paused its easing cycle after three cuts and pivoted hawkish as inflation proved sticky, while the Fed remained under political pressure and cut rates, widening the yield differential in Australia's favour.

However, positioning has become stretched. Non-commercial net longs have reached record territory among asset managers, raising the risk of violent unwinds on any negative catalyst. The familiar pattern of April played out repeatedly, the US would signal progress on Iran talks, the AUD would spike, Iran would deny the talks ever happened, and the move would partially reverse. AUD/USD ultimately drifted toward the 0.697 area mid-month before recovering as ceasefire hopes stabilised.

With markets now pricing an ~80% probability of a further RBA rate hike to 4.6% by August, driven by persistent inflation, the AUD looks fundamentally supported. But with the Strait of Hormuz still restricted and oil prices elevated, volatility is unlikely to subside quickly. For Australian businesses, this remains a currency requiring active management.

The AI Hardware Trade Is Back — With Force

The Philadelphia Semiconductor Index rose nearly 40% in a single month. Taiwan and Korea led global markets. The rotation is real.

After months of rotation away from high-multiple technology names amid geopolitical risk-off, April saw a violent reversal back into AI and the semiconductor supply chain. The catalyst was a combination of the ceasefire relief trade and a string of earnings beats from technology companies reaffirming the durability of AI infrastructure spending.

The Philadelphia Semiconductor Index rose close to 40% over the month alone, a staggering move that highlights just how deeply out-of-position many institutional investors had become. Taiwan and South Korea, home to the most critical nodes of the global AI chip supply chain; TSMC, Samsung, SK Hynix, were the standout equity markets globally for the month, with the MSCI EM Asia Index recouping all of its war-related losses and then some.

Earnings Season: Better Than Anyone Expected

84% beat rate. 27% EPS growth. The Magnificent 7 up 61%. Corporate America delivered — emphatically.

With approximately two-thirds of the S&P 500 having reported by month-end, Q1 2026 earnings season was shaping up to be a genuine standout. The beat rate of 84% was well above the long-run historical average of 73%, and consolidated earnings growth of 27.1% if sustained would represent the fastest pace since Q4 2021.

The Magnificent 7 remain the engine of consolidated growth, with EPS up 61% year-on-year. But, and this is increasingly important earnings growth ex-Mag 7 is running at a still-healthy 16%, suggesting the earnings expansion is becoming more broadly based. Q1 2026 marks the sixth consecutive quarter of double-digit consolidated EPS growth for the S&P 500.

Financials were another standout. Wall Street's major banks posted profits well above estimates, with Goldman Sachs recording its best quarter in years and Morgan Stanley's equity traders contributing to what analysts described as a record "windfall" across the major institutions. Elevated market volatility, a fixture of the geopolitical environment proved highly profitable for institutional trading desks.

The strong earnings backdrop provided a fundamental anchor for the equity rally, giving investors confidence that the ceasefire-driven risk-on move was backed by genuine corporate profitability rather than just sentiment. Q1 GDP growth came in at 2.0% annualised — up sharply from the 0.5% pace in Q4 2025, offering further evidence of economic resilience.

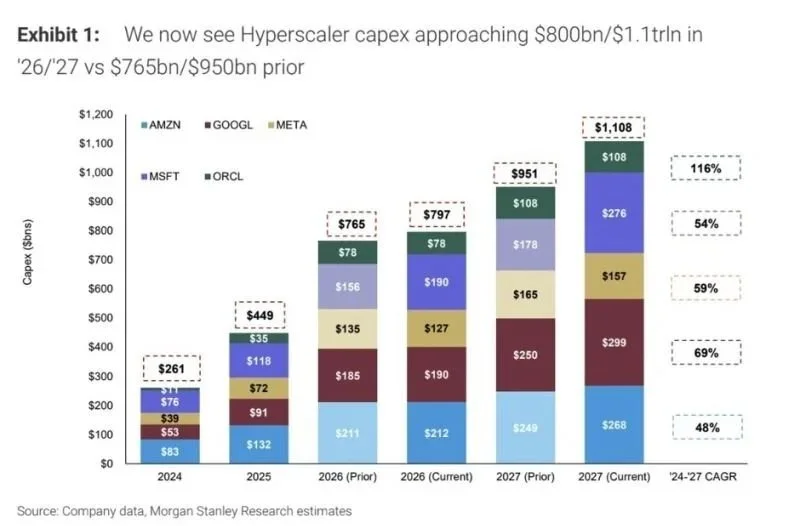

Capex Increase from the Hyperscalers

The biggest US tech firms now plan to spend as much as $725 billion this year on capital expenditures, primarily on AI data center equipment.

Morgan Stanley now sees hyperscaler capex approaching $800B / $1.1 trillion in 2026 / 2027 (versus $765B / $950B) prior. The ongoing ramp up in capex continues to drive AI hardware stocks higher; semicondictors, memory, indsutry stocks.