February Update

February 2026 marked a clear inflection point for global markets. What began as a relatively orderly rotation beneath the surface ended with a geopolitical shock that reshaped the macro outlook. By month-end, investors were no longer debating positioning or valuations — they were repricing risk.

Tech Cracks First: AI Optimism Meets Reality

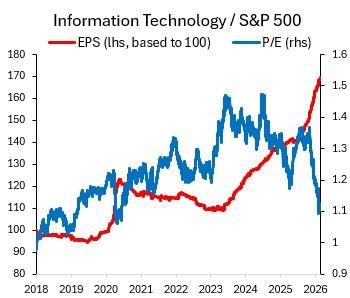

The defining feature of early February was a steady weakness in technology and software stocks. After a prolonged period of outperformance driven by AI enthusiasm, cracks began to emerge in the narrative.

However, the market reaction has become increasingly indiscriminate.

What’s being missed in the selloff is that AI does not replace software — it sits on top of it. These models require structured data, workflows, security layers, and integration into existing enterprise systems to function effectively. That infrastructure is owned and monetised by software platforms. In many cases, AI is more likely to increase usage, expand pricing models, and deepen customer dependence, rather than disrupt it.

Yet valuations across the sector have reset as if growth durability has structurally deteriorated.

This suggests the market is conflating short-term uncertainty around AI monetisation with long-term demand destruction. In reality, the shift from seat-based pricing to usage-based or consumption-driven models may introduce near-term noise, but it ultimately expands the revenue opportunity for high-quality platforms.

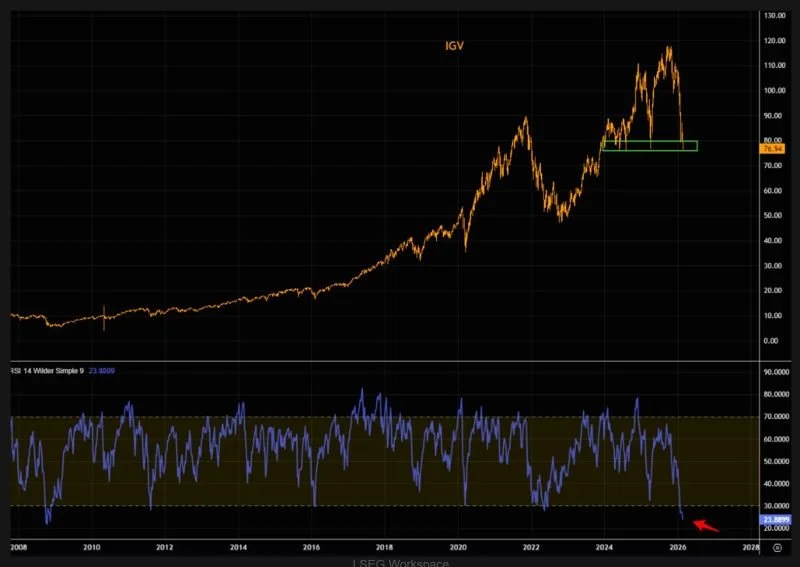

Software Heavily Overdone

Software is deeply oversold (see IGV ETF) .

Anthropic’s Enterprise Agents event reinforces that model providers are more likely to act as orchestration layers on top of incumbent software systems, not replace them, given the deep data, workflows, and metadata embedded in existing platforms (“Claude is only as useful as the data it connects to”). AI displacement risk to core software is over embedded in current multiples, making the event incrementally positive for the software sector. Risks remain, including pressure on software development costs, potential changes to the interaction layer that could lower switching costs, and increased competition around the “control plane” for agentic AI, though DB continues to see this dynamic as supportive for infrastructure and compute demand.

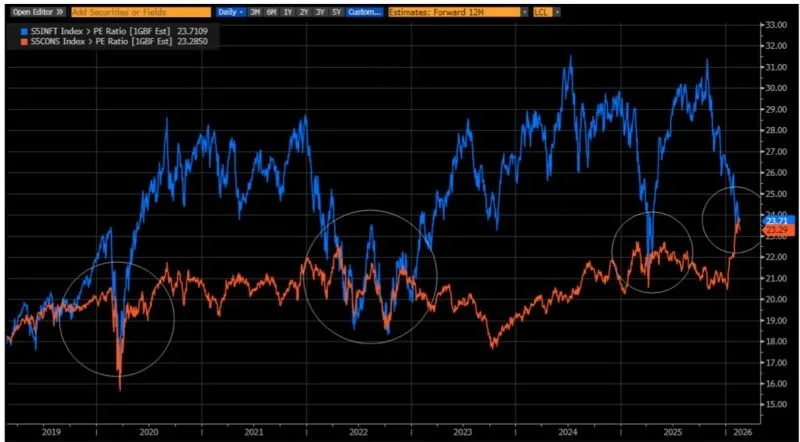

Tech Stocks Are Cheaper Than Consumer Staples

One of the clearest signs that the tech selloff is overdone shows up in valuations. The forward P/E of the tech sector has now compressed to parity with consumer staples, a move that makes little sense fundamentally. Tech companies are expected to deliver structurally higher growth and longer-duration cash flows, while staples are slow-growth, defensive businesses. Yet the market is pricing both the same.

Historically, this level of convergence has only happened three times in the past seven years: during COVID, the 2022 bear market, and the recent “Liberation Day” event — all periods of acute macro stress and indiscriminate selling, not structural deterioration in tech fundamentals.

The implication is clear: the market is aggressively repricing risk and underestimating the durability and growth potential of high-quality technology businesses. When a high-growth sector trades in line with slow-growth staples, it rarely reflects fair value — it signals that sentiment has overshot reality.

Geopolitics Builds — Then Breaks

Throughout February, geopolitical tensions involving Iran were steadily escalating. Markets were aware of the risks, but for most of the month, they were treated as a tail scenario rather than a base case.

That changed abruptly on February 28, with the outbreak of the 2026 Iran war.

As IG succinctly put it, the month “began with diplomatic brinkmanship and ended with war.” The shift from potential risk to realised conflict forced an immediate reassessment of global macro conditions.

The implications were significant. Oil markets, already sensitive to tensions in the region, now faced the prospect of supply disruption through critical chokepoints. This introduced a new layer of inflation risk at a time when central banks were already struggling to bring price pressures under control.

Higher oil prices reinforced inflation risks. Inflation risks reinforced the “higher for longer” rate environment. And that, in turn, compounded the pressure on long-duration growth assets.

The Reserve Bank of Australia delivered a rate hike during the month, reinforcing the “higher for longer” narrative around inflation and monetary policy.

This mattered for markets because higher rates disproportionately impact long-duration assets — precisely the segment where technology and software sit. As discount rates rise, the present value of future earnings declines, putting pressure on valuations.