In the Press: The Great Wealth Transfer & WealthTech

Huw Davies, Portfolio Manager, joined Ausbiz to discuss structural tailwinds in WealthTech. He highlighted rapid growth in global and Australian pension assets, declining adviser numbers, and the accelerating role of AI. Davies emphasised the Great Wealth Transfer—$3.5–$4.9 trillion in Australia and $84 trillion in the U.S.—driving demand for scalable, technology-enabled advice. Platforms leveraging rich data and AI, like Hub24, Netwealth and LPL are well positioned to capture this generational shift and deliver higher-quality, efficient client outcomes.

Watch Here: The well-placed ASX wealth platforms

WealthTech and AI: Reshaping the Future of Advice

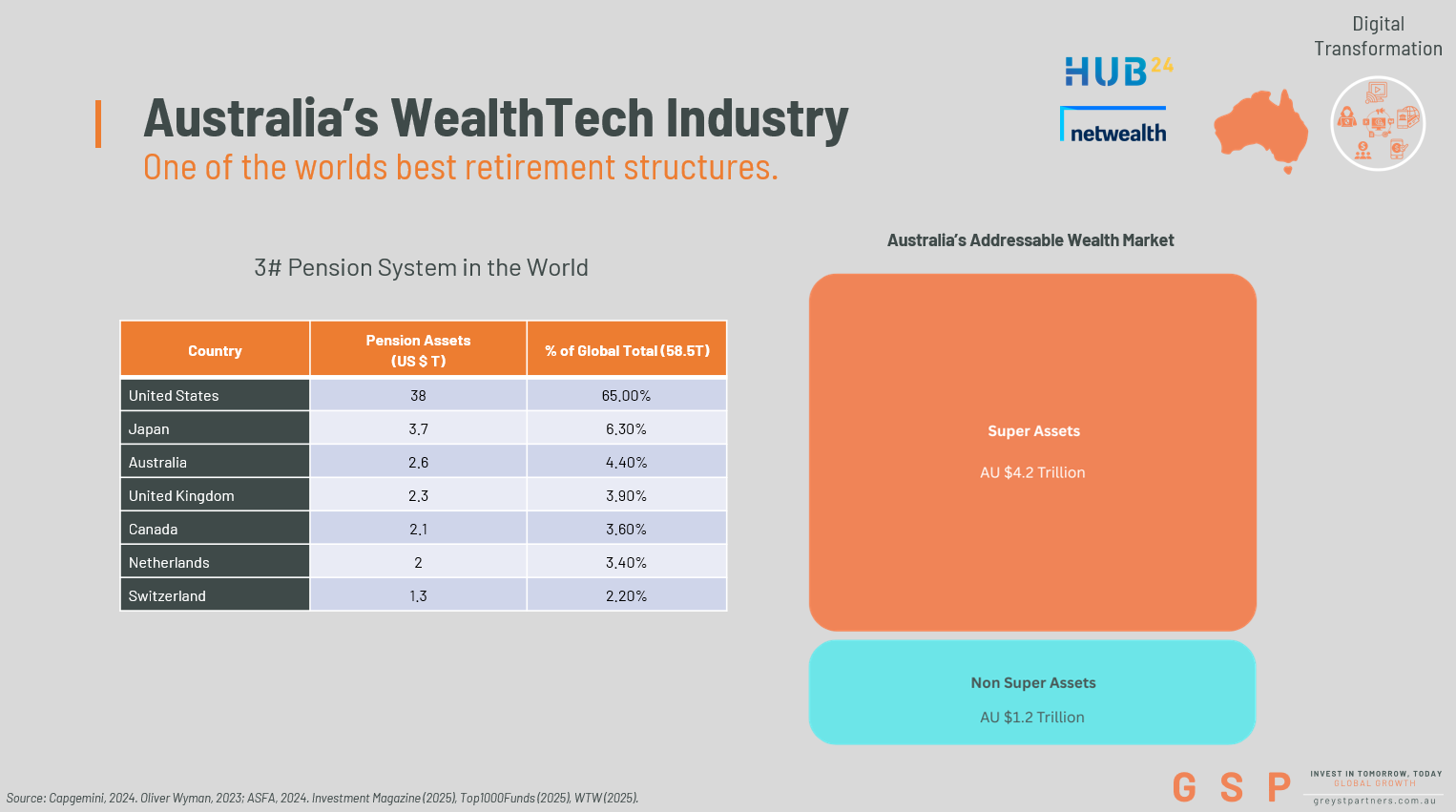

The global wealth management landscape is undergoing a structural transformation, driven by massive pension pools, intergenerational wealth transfers, and rapid advances in technology. In 2025, total pension assets across the top 22 markets reached ~US$68.3 trillion, up 9.5% year-on-year. The U.S. dominates with 66% of this total, reflecting a 7.7% CAGR over the last decade, while markets like South Korea, Switzerland, and Hong Kong have grown slightly faster. Australia’s superannuation system now holds roughly AUD $4.2 trillion (USD $2.6T), accounting for 4.4% of global pension assets, making it the fifth-largest system worldwide.

The Great Wealth Transfer: Australia and the U.S.

Australia

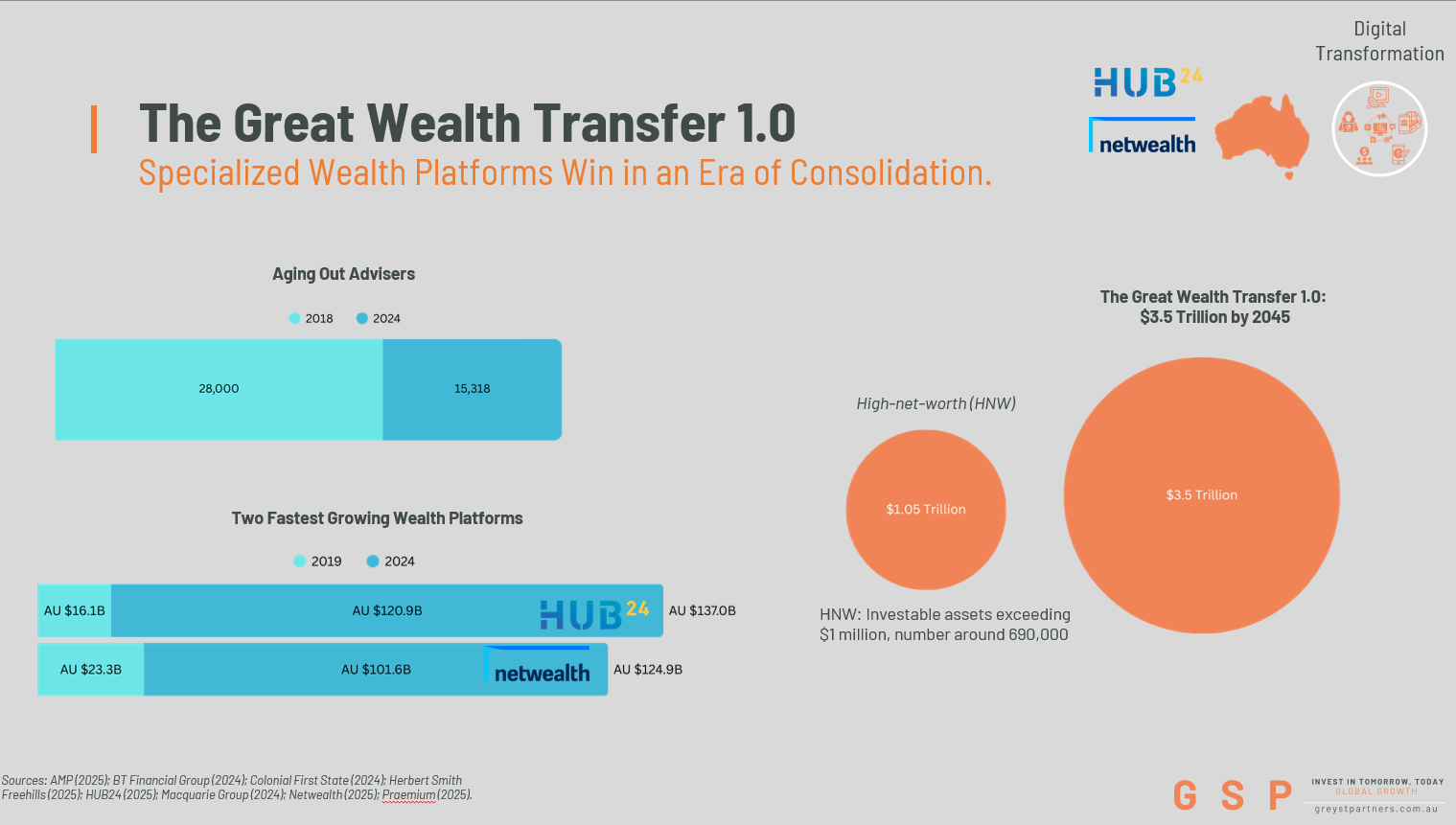

Australia’s wealth transfer dynamics are remarkable. The country has ~690,000 high-net-worth individuals (HNWIs) holding $1.05 trillion in investable assets, and over the next 20 years, $3.5 trillion is expected to pass to the next generation. However, the advice industry is consolidating rapidly: registered financial advisers fell from ~28,000 in 2018 to 15,318 in 2024, driven by regulatory pressure, aging advisers, and the exit of bank-affiliated advice post-royal commission. Fewer advisers are now managing more clients with increasingly complex needs, accelerating adoption of platforms and WealthTech solutions.

United States

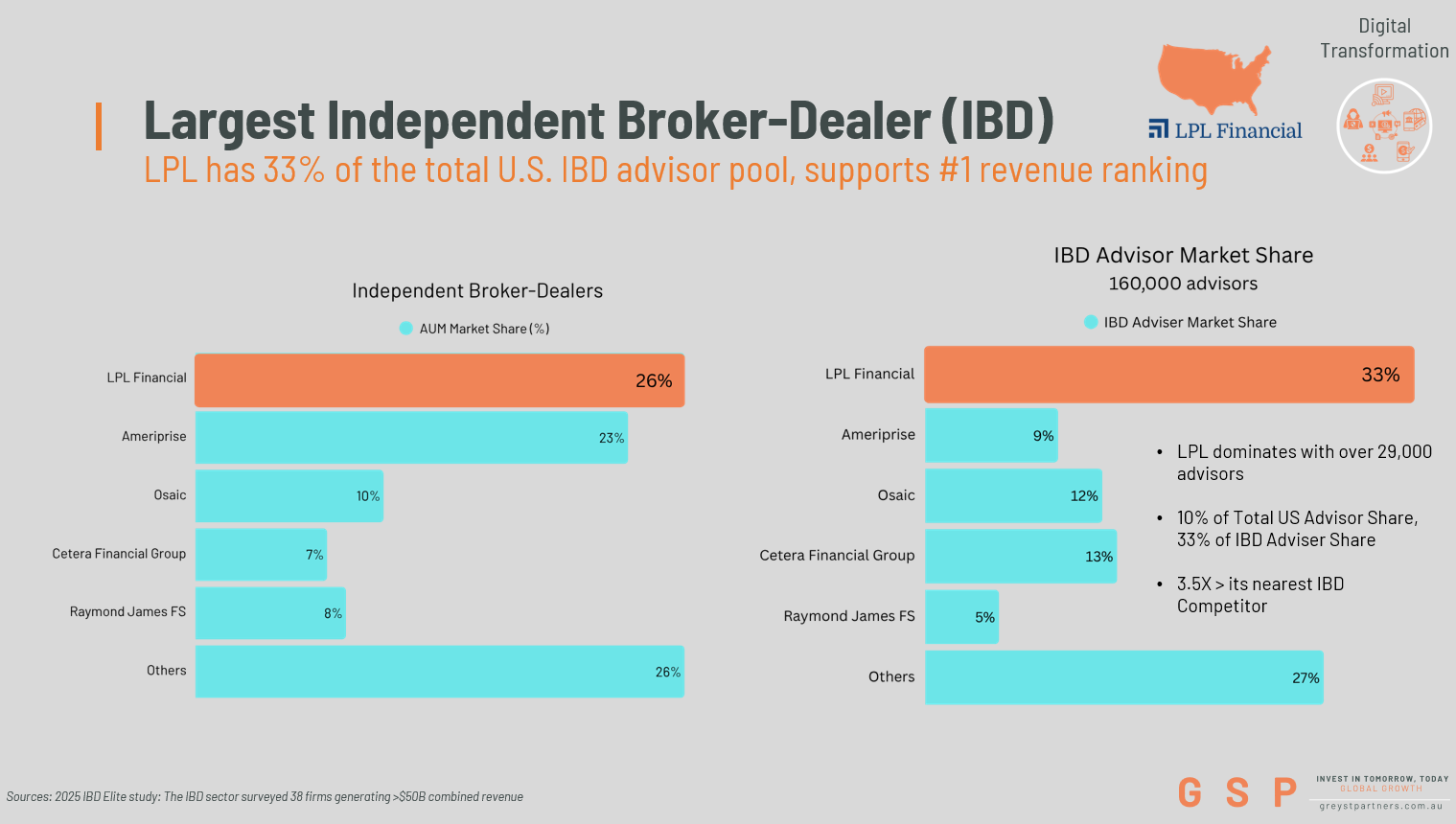

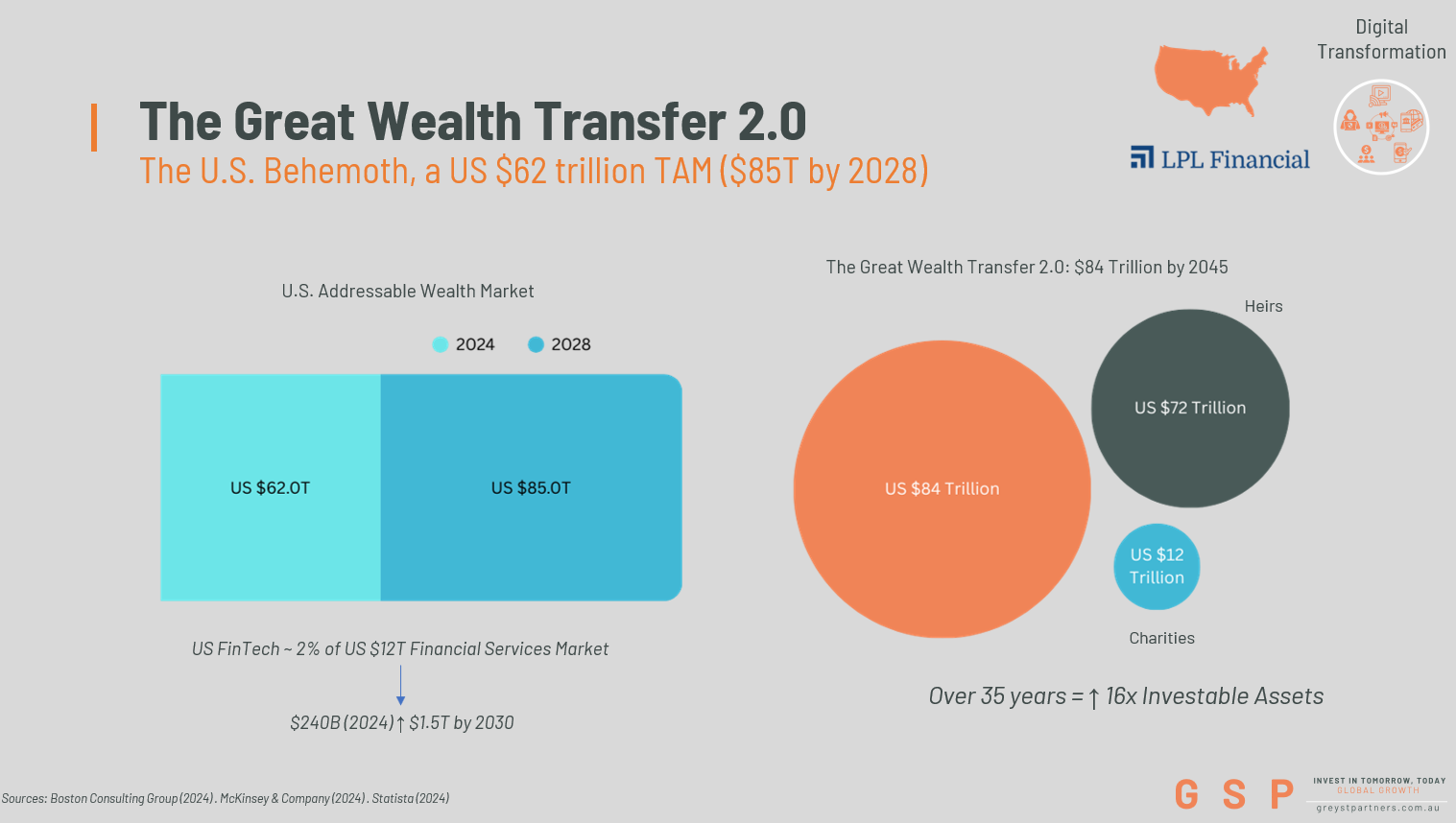

In the U.S., a multi-decade transfer of assets from Baby Boomers to Gen X and Millennials is reshaping advice consumption. Household net worth has quadrupled over 35 years, while investable assets have grown 16-fold. The industry currently manages ~$62 trillion in assets under management (AUM), projected to reach $85 trillion by 2028. Total financial advisors nationwide are estimated at ~300,000–322,000, spanning independent broker-dealers (IBDs), wirehouses, RIAs, insurance-affiliated, and self-employed channels. LPL Financial’s ~29,000 advisors represent ~10% of this total, while the IBD channel accounts for ~160,000 advisors, with LPL controlling ~18% of that segment. This scale positions advisor-led platforms to capture structural tailwinds from asset migration and multi-generational planning needs.

AI: Moving Up the Value Chain in Wealth Management

Artificial intelligence is increasingly shifting from basic support tasks to high-value advisory functions. In the U.S., Altruist’s Hazel AI exemplifies this transition, automating complex tax planning and moving beyond rudimentary assistant functions like transcription. Hazel AI does not replace advisers—it eliminates low-value labor and workflow bottlenecks, enabling more accessible, affordable, and higher-quality advice.

The impact is clear: AI addresses two major pressures in the wealth industry—adviser productivity and client expectations for digital engagement. However, its effectiveness depends on integrated platforms that consolidate administration, reporting, trading, and advice delivery. Without these systems, AI cannot scale efficiently.

How AI Enhances Wealth Platforms

AI integration strengthens platforms across four areas:

Research & Investment Analysis – Large language models analyze filings, transcripts, and alternative data, producing actionable insights faster than manual workflows.

Adviser Augmentation – AI copilots reduce drafting time for Statements of Advice, allowing advisers to focus on strategy.

Operational Automation – Onboarding, reconciliations, and compliance monitoring become faster, cheaper, and more accurate.

Personalized Engagement – Chat assistants and robo-advice deliver client responsiveness at scale.

Proprietary data is critical: platforms with rich client and portfolio datasets can train AI models that provide differentiated, high-quality outcomes.

Platform Leaders and Market Opportunity

Australia

Hub24 (ASX:HUB): AU$152.4B funds under advice (FUA), ~9% market share, 5,200 adviser users, AU$19.8B net inflows FY25.

Netwealth (ASX:NWL): AU$125.6B FUA, ~9% market share, 4,089 adviser users, 172,221 accounts.

Both platforms have experienced share price drawdowns but continue to show strong growth trajectories, with market share gains projected to 16% by 2030.

United States

LPL Financial (LPLA): $2.4T in assets, ~29,000 advisors (~10% of total U.S. advisors), 26% of IBD AUM, ~78% of advisors adopting or planning AI tools. LPL focuses on capacity creation and adviser efficiency, rather than disintermediation, delivering 22–24% revenue growth potential.