In The Press: Ausbiz - ETFs to play the tech rotation

6th July 2026

Daniel Reaper, Portfolio Manager, joined AusbizTV to discuss how Tech leadership consolidating rather than undergoing a full regime change. Markets love a good narrative, and the dominant one of the past 18 months has been narrow leadership driven by the Magnificent 7 and hyperscalers. Recent price action has prompted plenty of headlines about “rotations” and regime change. In our view, that framing overstates what is happening. What we are seeing is a healthy consolidation and digestion phase, not the end of prior leadership, but a necessary rebalancing within it.

Watch Here: ETFs to play the tech rotation

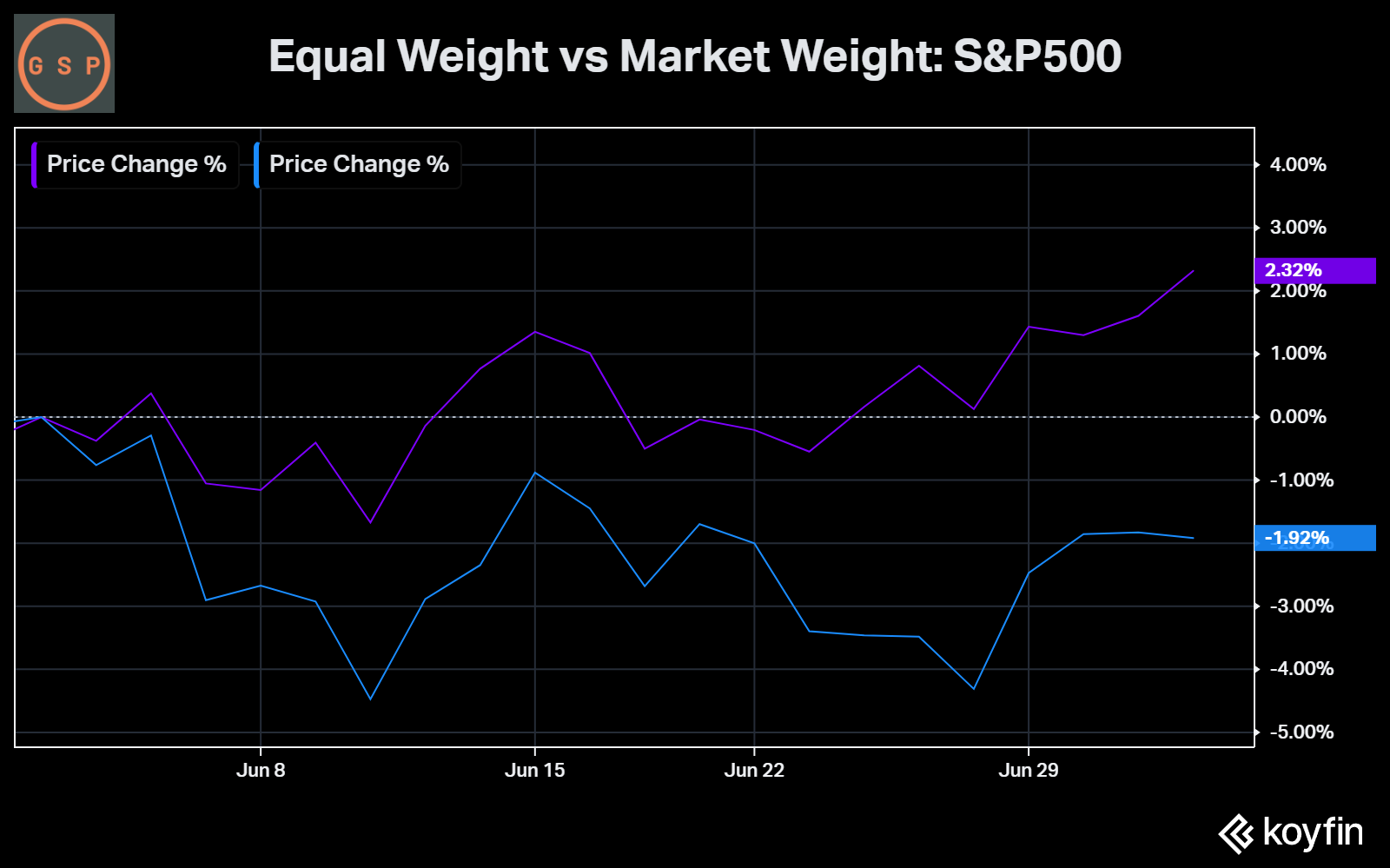

June's Breadth Signal

June delivered one of the clearest improvements in market breadth in months. The equal-weighted S&P 500 ETF (RSP) gained about 2% while the cap-weighted S&P 500 (IVV) fell nearly 2%, creating a 4% performance gap in a single month. The Mag 7 declined 5 to 6% and erased close to $3 trillion in market value, with the MAGS ETF posting one of its weakest months on record. For a long time the market has been narrow, with the Mag 7 and hyperscalers driving almost all gains. These stocks still account for around 25% of forward S&P 500 earnings and about 14% of total revenue next year. What we are seeing is some of that concentration beginning to unwind in an orderly way. This looks like a healthy digestion phase rather than a full change in market leadership, creating a classic opportunity to add to quality names on weakness.

The Capex Rotation: Cheque Writers to Cheque Receivers

The more important dynamic is where capital is flowing. Hyperscalers have entered a heavy capex phase, directing record spending toward semiconductor and memory companies. Semiconductors have grown from roughly 2% of the S&P 500 a decade ago to around 20% today and have driven more than half the index's year-to-date gains. The SOXX ETF remains up 88% YTD after peaking near 120%.

Goldman Sachs baskets capture the divergence clearly. The AI Semis basket reached 271 while the core hyperscalers basket closed June at 96, down 18% for the month and its worst performance since META's IPO. Memory now makes up about 25% of the bill of materials. This is pushing hyperscaler capex above $750 billion this year and over $900 billion next. Rising memory costs are pressuring near-term margins even as long-term free cash flow forecasts to 2030 remain solid. The move is targeted rather than a broad risk-off event.

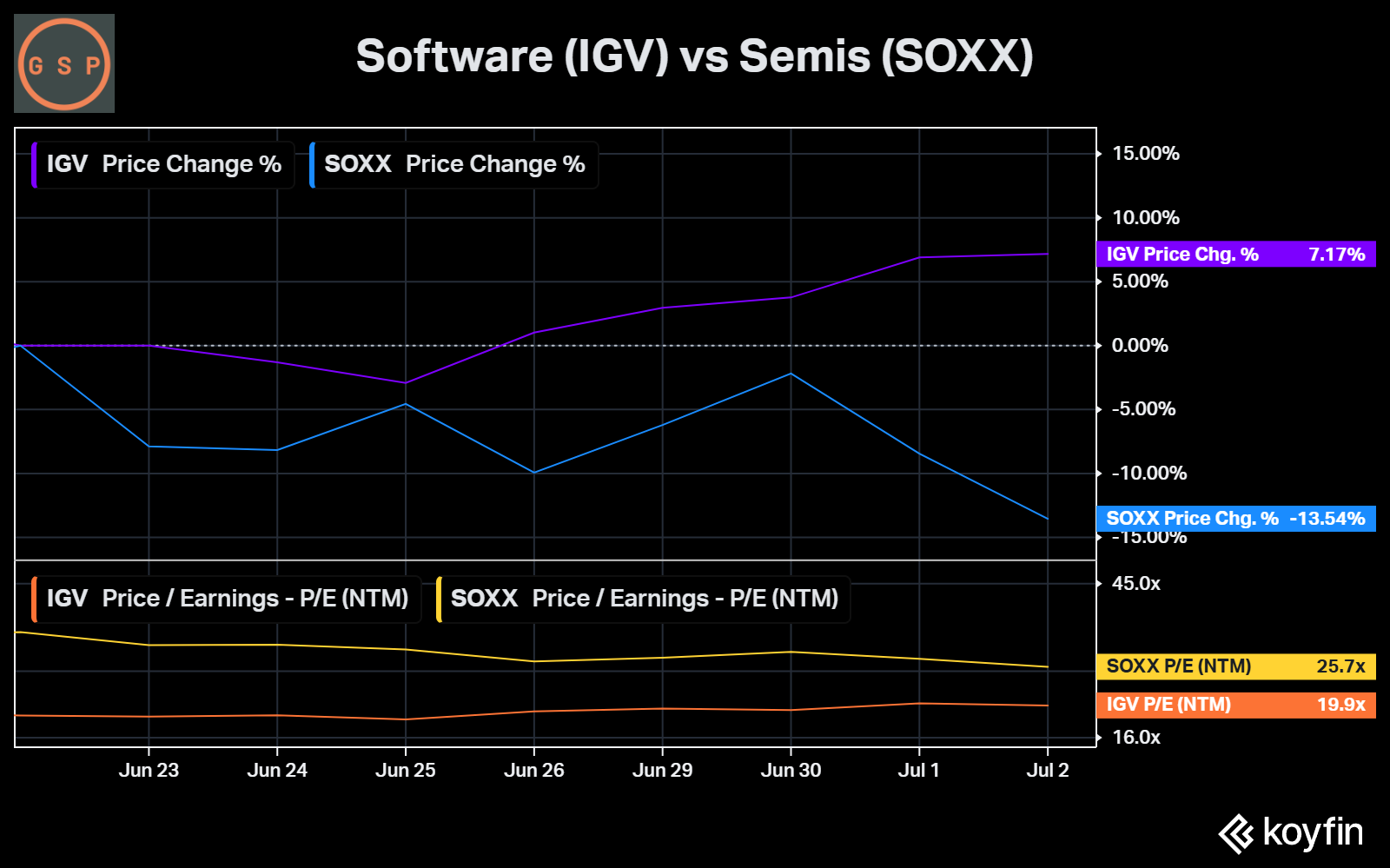

Software Offers Relative Value

Within technology we are also seeing rotation from semiconductors into software as the two baskets have turned negatively correlated. Over the past month the IGV software ETF rose around 7% while SOXX fell about 8%, a 15% differential. More recently SOXX is down nearly 12% while IGV is up 3%.

Software had been heavily sold off, with many names down nearly 35% from their highs and RSI readings below 30. We expect the sector to become more range-bound and act as a relative value trade when semiconductors heat up again. The names we hold and watch closely include ServiceNow, Salesforce, Oracle, Intuit and Palantir, with Microsoft behaving similarly to the broader software group.