Why Michael Burry is Wrong

6th July, 2026

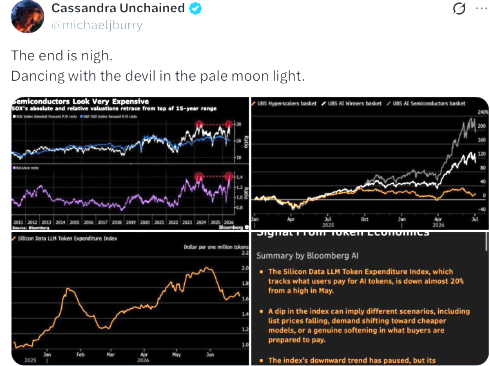

Michael Burry is back with one of his signature dramatic posts.

“The end is nigh. Dancing with the devil in the pale moon light.”

The charts he shared are striking. It shows semiconductor valuations near 15-year highs on both absolute and relative terms, hyperscaler and AI semiconductor baskets ripping higher while the Silicon Data LLM Token Expenditure Index has rolled over ~20% from its May 2026 peak, and a Bloomberg summary highlighting weakening pricing signals.

Burry has put real money behind the view. He recently disclosed fresh short positions in Nvidia, Tesla, Caterpillar, Applied Materials, and the iShares Semiconductor ETF (SOXX) via long-dated puts. His base case points to a 30–40% market correction by March 2027.

His core argument is simple and provocative:

The companies buying the AI infrastructure (Microsoft, Amazon, Google, Meta) have seen relatively modest stock returns this year, while the companies selling the picks and shovels have surged more than 200%. If the customers aren’t yet earning strong returns on their massive spending, who ultimately justifies these valuations?

He adds several warning signs:

The Philadelphia Semiconductor Index (SOX) trading ~65% above its 200-day moving average — levels last seen in March 2000.

Forward P/E ratios for semis near ~30x, at the top of the 15-year range.

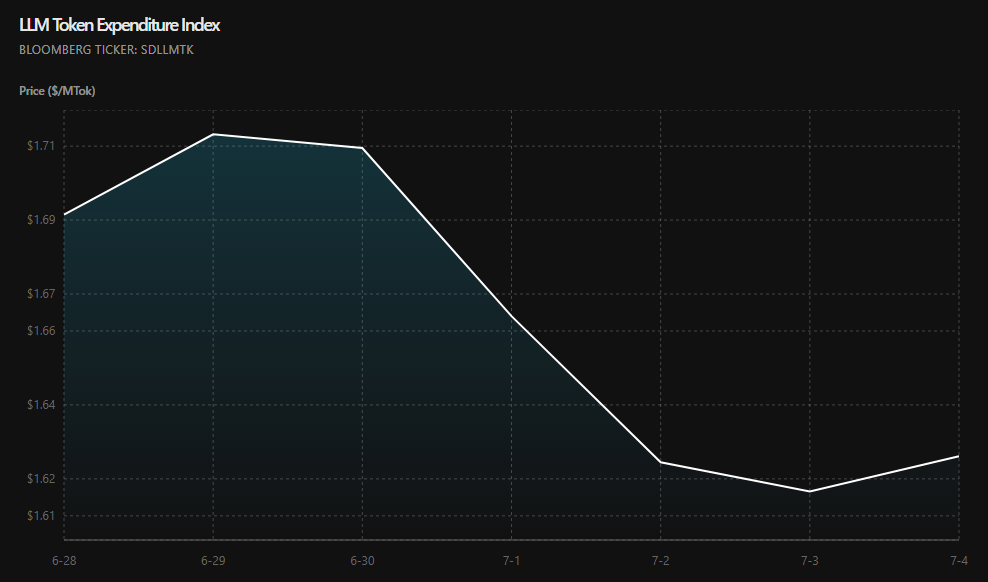

AI token pricing (via the Silicon Data LLM Token Expenditure Index) already down nearly 20% from the May peak.

Hyperscalers allegedly understating depreciation by ~$176 billion between 2026–2028 by extending useful lives of AI hardware beyond realistic 2–3 year cycles.

Where Burry Has a Legitimate Point

Burry is right to force the question of returns, not just narrative. Capex at the hyperscalers has exploded. Valuations in the semiconductor complex are undeniably stretched on traditional metrics. The Token Expenditure Index decline is real and worth watching it reflects what the market is actually willing to pay for LLM inference right now.

The depreciation point is also substantive. If companies are systematically extending asset lives on rapidly evolving GPU technology, reported earnings could be inflated in the near term, with a catch-up effect later. That’s a legitimate accounting debate.

Why Burry Continues to Miss the Mark

Here’s where the “broken clock is right twice a day” analogy applies.

Burry was spectacularly right about the 2008 housing bubble. But on technology and growth cycles, he has a long track record of being directionally early sometimes very early and missing the magnitude and duration of the move higher.

Several things weaken the immediacy of his current call:

1. The Token Expenditure Index decline is not the smoking gun.

The index fell because of a usage mix shift toward cheaper models (including open-weight options), not purely because list prices collapsed across the board. Silicon Data themselves have noted that movements are heavily driven by where actual expenditure is flowing. When users optimize toward more efficient or lower-cost models, the blended rate drops, but total token volume can still rise significantly. This is classic Jevons Paradox in action: cheaper unit costs unlock more usage. Multiple analysts (including Citadel Securities) have pointed out that falling token prices do not necessarily contradict rising infrastructure demand in an elastic market. Total spend on AI inference has continued to grow even as unit economics improved.

2. The “buyers aren’t earning returns yet” argument is premature.

Hyperscalers are building platform capabilities that take years to fully monetize, not just buying GPUs for today’s workloads. Much of the current spend is foundational (training clusters, inference capacity, new product development). The real earnings leverage often shows up 18–36 months later through cost savings, new AI-powered products, and cloud pricing power.

Comparing 2025–2026 stock performance of buyers vs. sellers also ignores that many hyperscalers were already expensive and had other headwinds. The infrastructure sellers had more torque to the pure AI narrative.

3. Depreciation schedules are an accounting judgment, not obvious fraud.

Burry is correct that hardware turns over quickly. But companies have always had incentives (and precedent) to use longer depreciation lives for technology assets, and auditors have signed off. The $176 billion figure is his estimate, big, but not universally accepted as a near-term earnings cliff. Actual replacement cycles are evolving with better utilization, software optimization, and newer chip architectures.

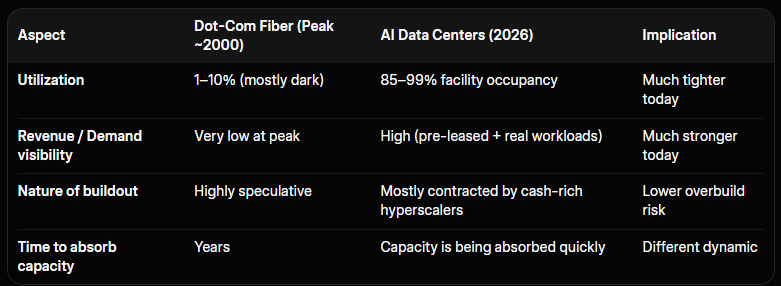

4. The dot-com parallel has limits and is lazy.

Yes, valuations are high and concentration is high. But today’s leading AI companies have real revenue, real earnings, and real (if early) product-market fit at massive scale. The 2000 bubble had far more companies with no revenue and no path to profitability. The current cycle also features genuine geopolitical and competitive drivers (U.S.–China tech competition) that were absent in 1999–2000.

The Broken Clock Problem

Michael Burry is one of the sharpest macro thinkers of his generation. When he speaks, markets sometimes listen. But his style dramatic, binary, and often early means he frequently misses the middle innings of major technological shifts.

He was early on the post-GFC recovery. He has been consistently skeptical of the AI buildout for some time while the market has priced in accelerating adoption. Being right on the eventual need for mean reversion does not mean being right on when or how violently it arrives.

The Real Debate

The most valuable part of Burry’s intervention isn’t the prediction of imminent doom. It’s the shift in conversation from “AI is transformative” to “What are the actual returns, and when do they show up?”

That is the right question. The Token Expenditure Index, hyperscaler free cash flow trends, and actual monetization metrics will matter far more over the next 12–24 months than dramatic tweets.

A broken clock is right twice a day. Michael Burry might eventually be right about the excesses in parts of the AI trade. But history suggests he is more likely to be early than precisely timed — and that the market can remain irrational (or rationally optimistic) longer than even the smartest bears expect.

The end may not be as nigh as the pale moonlight suggests. But the scrutiny on returns is only just beginning.