In the Press - Ausbiz TV: Opportunities amidst the SaaS-pocalypse

Daniel Reaper, Portfolio Manager, joined Ausbiz TV to discuss the so-called “SaaS apocalypse” and whether AI represents threat or opportunity. He argues that while AI agents are reshaping workflows and challenging per-seat licensing models, the market reaction has been excessive. High-quality platforms embedded at the core of enterprise operations remain difficult to displace. With valuations well below long-term averages, leaders such as Salesforce, Oracle and ServiceNow are positioned to monetise AI rather than be disrupted by it, creating compelling long-term opportunities amid widespread fear and indiscriminate selling across the sector.

Watch: Opportunities amidst the SaaS-pocalypse

The “SaaS-pocalypse” — Or a Generational Opportunity?

Right now, the market doesn’t know who the winners of AI will be — so everyone is being treated like a loser.

It’s a classic shoot-first, ask-questions-later moment.

The sell-off began in October and accelerated in January following the preview of Anthropic’s Claude Cowork. Unlike a simple chatbot, Claude demonstrated autonomous agents capable of executing complex workflows with minimal human input. That sparked a critical question: if one AI agent can do the work of five to ten employees, what happens to the traditional per-seat SaaS model?

For decades, software revenue scaled with headcount. More employees meant more licenses. Valuation multiples assumed hiring growth would continue. But if agentic AI reduces the need for employees, that implies fewer seats and potentially a smaller revenue base — hence the sharp compression in multiples.

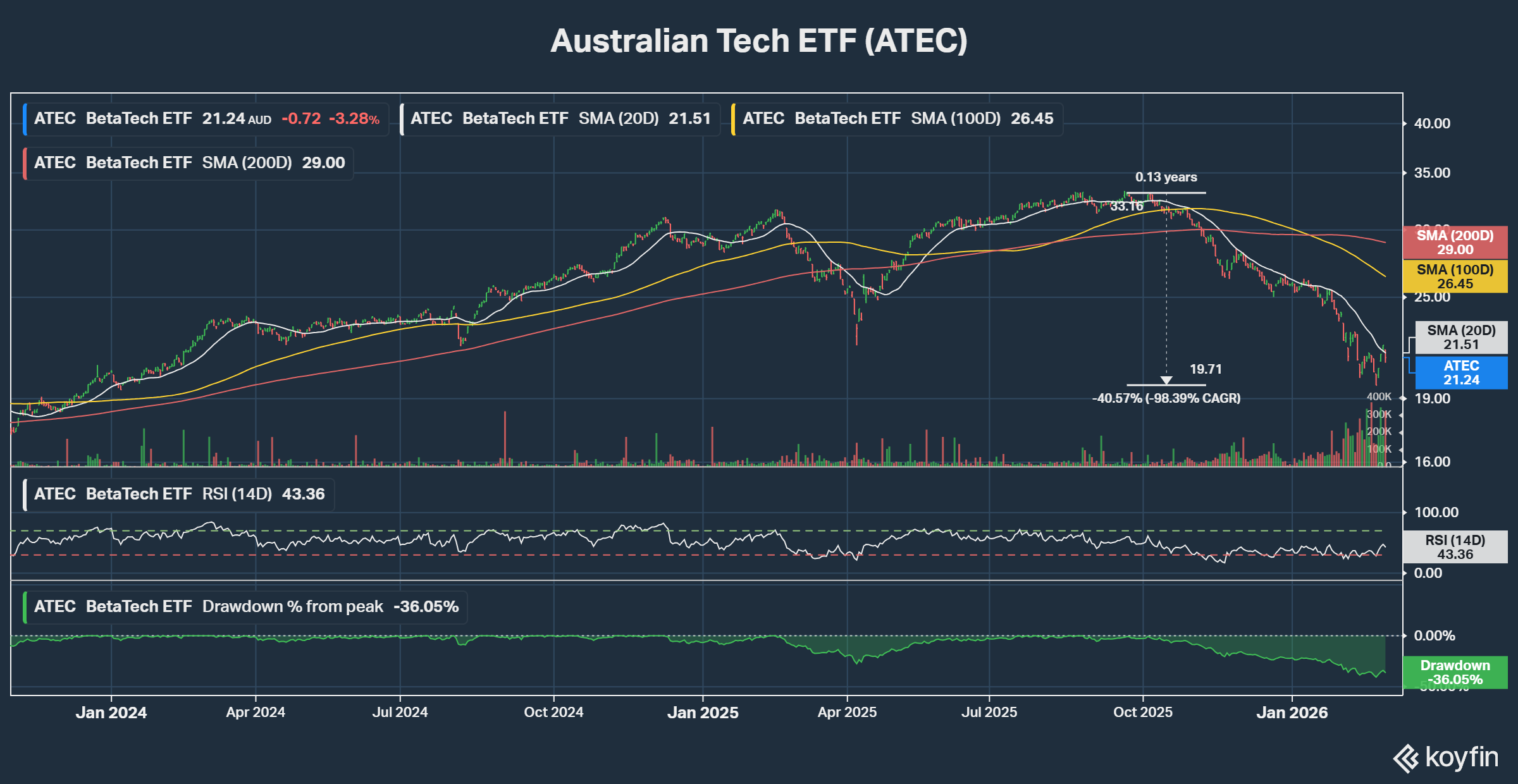

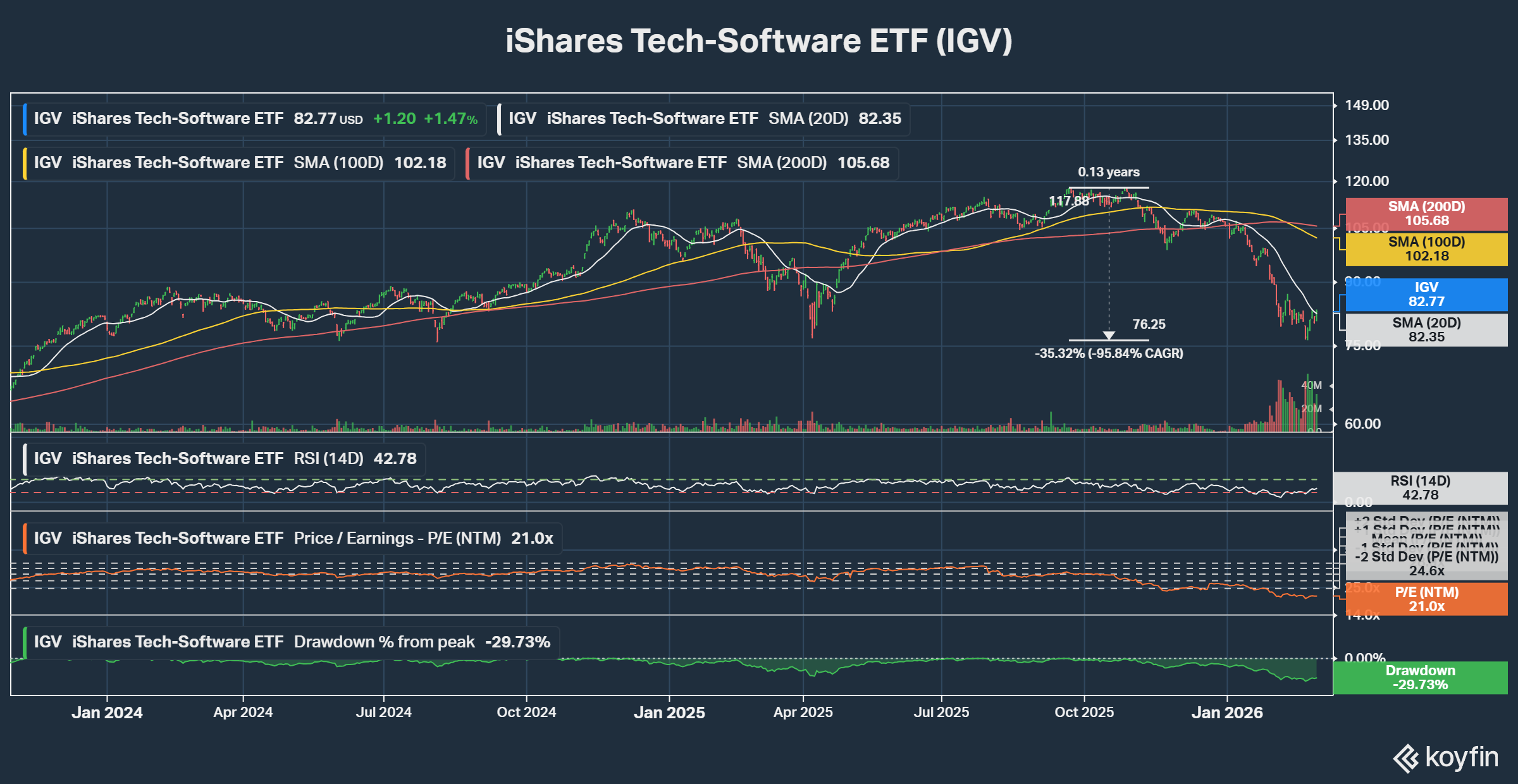

This isn’t a typical cyclical downturn like 2021–22, when the Nasdaq-100 fell nearly 40%. Today’s pressure feels structural, particularly across long-duration growth names. The Australian tech index is down over 40% from its highs. In the US, the IGV software ETF is roughly 30% off its October peak, trading at around 20x forward earnings versus a ten-year average of 34x — nearly two standard deviations below the mean. February even recorded the most oversold 14-day RSI in US software history, worse than 2001.

Hence the term “SaaS-pocalypse.”

But this is not the end of software.

Where We See Opportunity

Our focus is simple: own platforms that control mission-critical workflows.

Salesforce is trading around 15x forward earnings, Oracle around 20x, and ServiceNow roughly 26x — despite strong projected earnings growth. For context, Coca-Cola trades near 25x with low single-digit growth. There is clear valuation asymmetry in high-quality software.

These are not casual subscriptions. They are the operating systems of large enterprises.

Salesforce’s data and workflows are deeply embedded. AI solutions are being built on top of the platform, not around it. The company has invested in AI since launching Einstein in 2017 and more recently introduced Agentforce, which is scaling rapidly. It also distributes AI solutions via its AppExchange ecosystem, enabling both internal and third-party innovation. AI is an enabler.

Oracle already has direct relationships with the world’s largest enterprises — banks, hospitals, governments — many of whom cannot simply hand sensitive data to unproven startups. The path of least resistance is embedding AI inside the trusted database and cloud stack they already use. Oracle is doing exactly that, integrating AI across its infrastructure while leveraging a substantial cloud backlog.

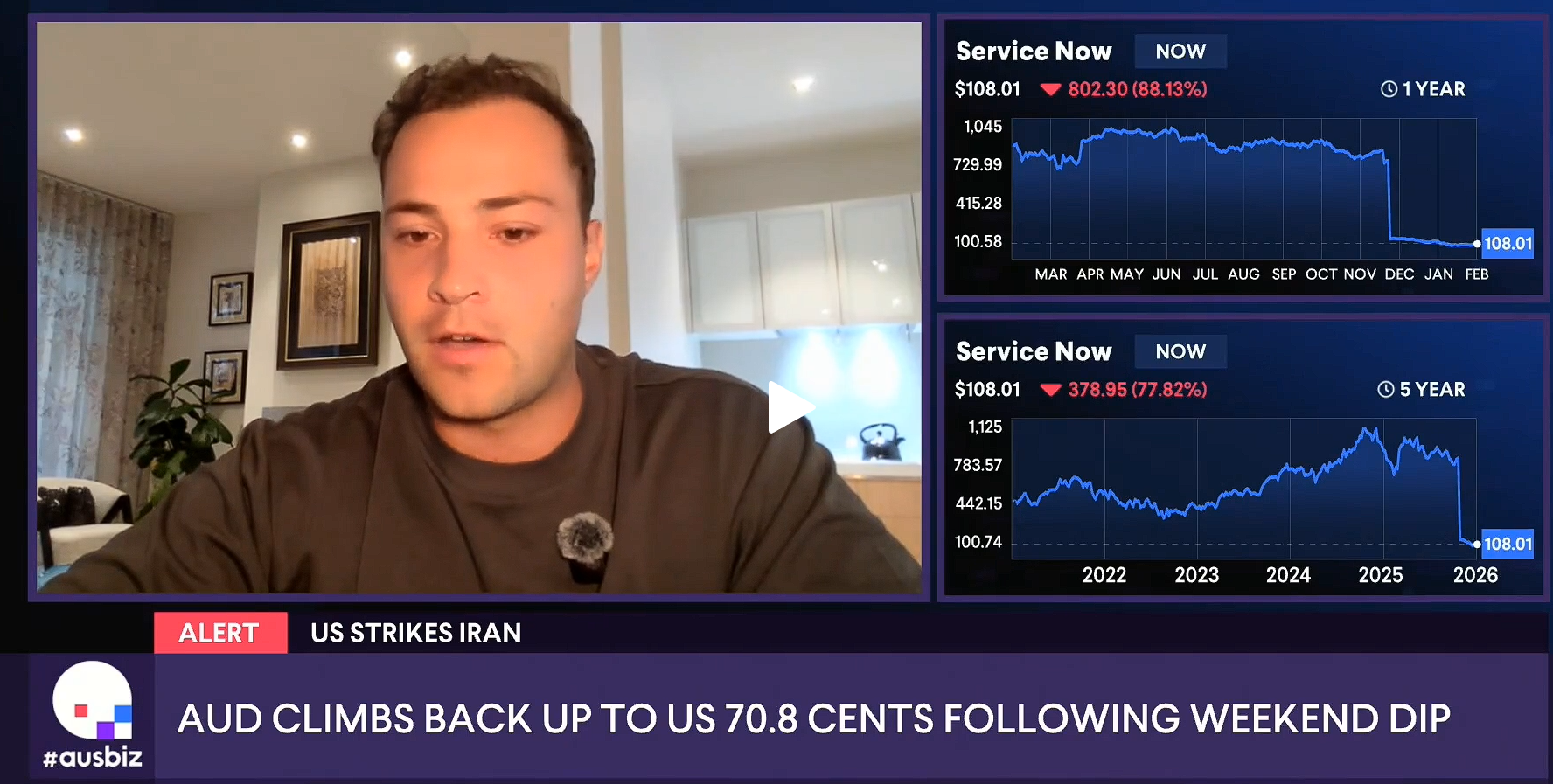

ServiceNow, with over 40% market share in IT service management, continues to roll out AI modules while maintaining near-perfect renewal rates. It is also experimenting with hybrid pricing — subscription plus usage — reflecting how monetisation models may evolve, much like the shift from perpetual licenses to SaaS years ago.

The Bigger Picture

When we step back, the story becomes clear.

The platforms that control enterprise data and workflows are not standing still. They are integrating AI. They are monetising AI. And they already own the distribution.

In a market pricing widespread disruption, we see durable incumbents adapting — and potentially emerging stronger.

That’s not a SaaS apocalypse.

That’s a once-in-a-generation opportunity.