Mini Series: A New World Order: Unsustainable Debt Cycles

Unsustainable Debt Cycles: The Pillar That Topples Empires

Today we’re diving into one of the four pillars that determine the rise and fall of empires:

Unsustainable debt cycles.

This forms part of our A New World Order mini-series, where we unpack the structural forces reshaping global power.

And right now, we are transitioning out of a 40-year era defined by falling interest rates, cheap money, and suppressed volatility — into something far less stable.

At the centre of that shift sits one variable: debt.

The 40-Year Tailwind: Falling Rates and Expanding Leverage

From the era of Paul Volcker in the early 1980s, interest rates began a structural decline. After double-digit inflation was crushed with aggressive tightening, the following decades were characterised by progressively lower borrowing costs.

Every slowdown — from the dot-com crash to the 2008 financial crisis and the COVID-19 shock — was met with cheaper money.

By the time we reached the aftermath of the Global Financial Crisis and later the pandemic, policy rates had fallen to zero or near-zero.

Cheap capital fuelled:

Asset price expansion

Government spending

Corporate leverage

Household borrowing

Financial engineering

But it also embedded leverage deep into the system.

Debt was manageable because interest rates were low.

The moment rates rise, the equation changes.

The End of Easy Money

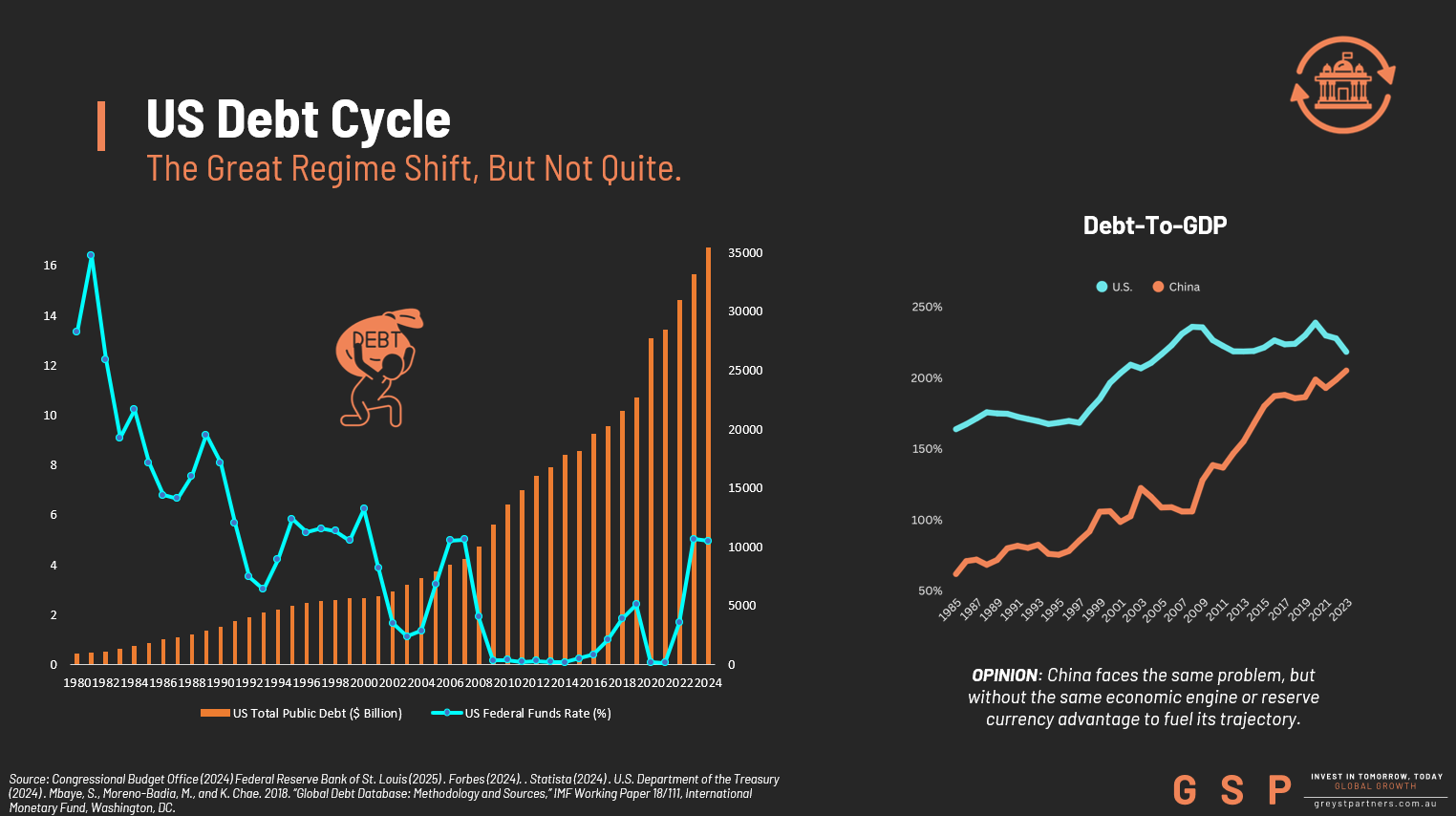

According to the U.S. Department of the Treasury, U.S. public debt has now surpassed $38 trillion. For years, servicing that debt was relatively painless due to suppressed yields.

The Federal Reserve played a major role in this dynamic.

Through quantitative easing, it absorbed massive bond issuance, stabilised markets, and effectively capped borrowing costs. Central bank balance sheets expanded dramatically after 2008 and again during COVID.

But that era of artificial liquidity has ended.

Rates have reset higher.

Quantitative tightening has replaced quantitative easing.

Bond markets are once again required to absorb issuance without guaranteed central bank support.

When borrowing costs reset, debt stops being abstract — and starts constraining policy.

This is the defining feature of late-stage debt cycles.

The Long-Term Debt Cycle

For decades, declining rates masked structural imbalances.

Initially, high rates under Volcker stabilised inflation.

Then successive cycles of easing stimulated growth.

Eventually, by the 2010s, rates hit the zero lower bound.

With traditional tools exhausted, central banks turned to balance sheet expansion.

The result?

Record public deficits

Surging sovereign debt

Elevated corporate leverage

Asset inflation across equities and property

Now, the supply of government bonds is surging just as central banks withdraw liquidity.

That creates a structural supply-demand imbalance — particularly in reserve currency nations.

And history suggests this phase rarely ends quietly.

Empires Rarely Fall From One External Rival

Empires do not typically collapse because of a single challenger.

They falter when internal debt erodes flexibility.

When interest payments crowd out productive spending.

When fiscal policy becomes constrained.

When monetary policy is trapped between inflation and solvency.

Debt reduces optionality.

And optionality is power.

The China Parallel

But here’s where the narrative gets more complex.

The supposed rising power — China — faces similar structural pressures.

Heavy property-sector leverage

Elevated local government debt

A shrinking working-age population

Persistent youth unemployment

The Chinese property downturn has been a multi-year drag on growth. Local governments have relied on land sales and leverage to sustain activity. Demographics are turning negative.

Both giants are leveraged.

Both face structural headwinds.

But only one issues the world’s primary reserve currency.

And that matters.

The Reserve Currency Advantage

The United States still benefits from dollar dominance.

The U.S. Treasury market remains the deepest and most liquid pool of sovereign capital globally. The dollar underpins global trade, reserves, and financial plumbing.

That reserve status provides:

Structural demand for U.S. debt

Lower relative borrowing costs

Greater policy flexibility

China does not yet enjoy that privilege.

Which means the contest is not simply about who has debt — both do.

It is about who retains flexibility within a leveraged system.

A Stress Test, Not a Handover

This is not a simple zero-sum handover of power.

It is a stress test of two highly leveraged systems operating in a new rate regime.

The long-term debt cycle appears to be turning.

The monetary order is under strain.

Liquidity is no longer expanding freely.

In highly leveraged environments, survival does not go to the strongest headline economy.

It goes to the most flexible.

The question is not whether debt matters.

It’s who can manage it without losing policy control.

And that’s the defining challenge of the next decade.