Mini Series: Black Gold - The Real Crisis is the Global Diesel Shortage

Crude oil comes in many forms, and where it comes from determines how it’s extracted—and how useful it is.

In parts of the Middle East, particularly Saudi Arabia, oil flows relatively easily from shallow reservoirs. In the United States, much of it is locked in shale rock and must be fractured out using hydraulic pressure. Canada produces oil from sands—energy-intensive and costly—while countries like Brazil and Norway drill deep beneath the ocean floor in complex offshore operations.

Not all oil is created equal. Some is “light and sweet”—easy to refine and low in sulfur. Other barrels are “heavy and sour”—thicker, dirtier, and more complex to process. This distinction matters more than most people realise, because it dictates how oil flows through the global system.

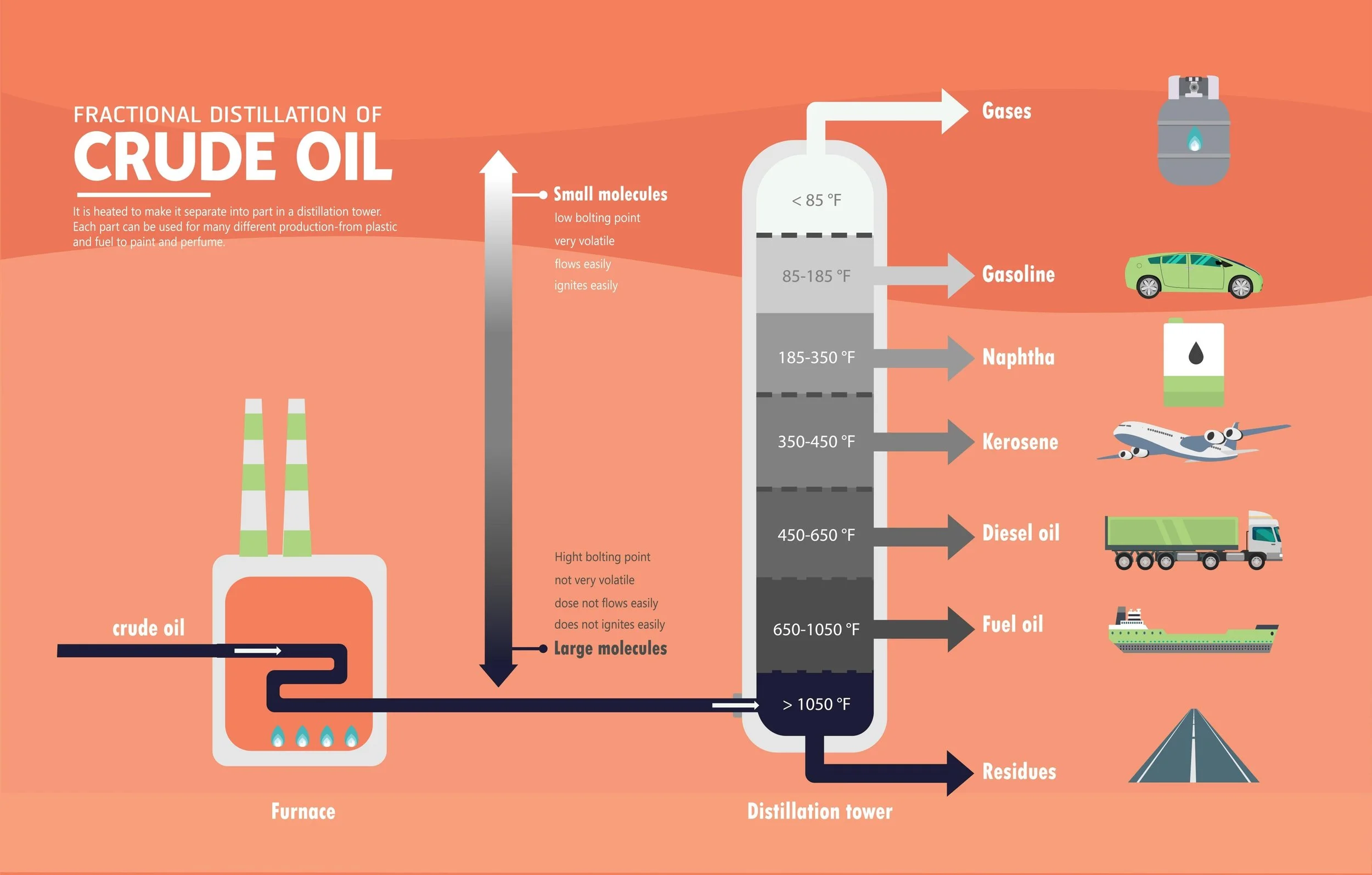

Turning Crude Into Something Useful

Raw crude oil, on its own, has limited use. Its real value emerges through refining—a process that separates hydrocarbons based on their boiling points.

Inside a refinery, crude is heated and split into layers:

Petroleum gases (5–10%) – used for heating and cooking

Naphtha (5–15%) – a key input for plastics and pharmaceuticals

Gasoline / petrol (40–45%) – the backbone of personal transport

Kerosene / jet fuel (8–12%) – essential for aviation

Diesel (25–30%) – the workhorse of the global economy

Heavy fuel oils (5–10%) – powering massive container ships

Residue – used for asphalt and road construction

This breakdown highlights something critical: diesel is not just another fuel. It underpins freight, agriculture, mining, and industrial activity. When diesel supply tightens, the real economy feels it immediately.

The Refining Imbalance

Here’s where things get more complex.

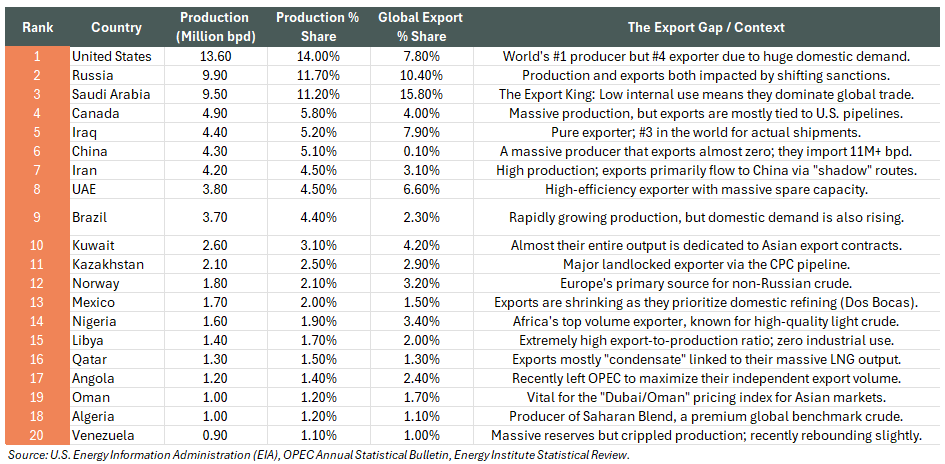

Some countries refine more oil than they produce. The United States is a perfect example—it produces roughly 14 million barrels per day, yet refines over 17 million. That imbalance exists because many U.S. refineries were built decades ago to process heavy crude from countries like Canada, Mexico, and Venezuela.

But U.S. production today is dominated by light sweet crude. So instead of using all its own oil domestically, the U.S. exports lighter barrels and imports heavier ones to keep its refining system running efficiently.

It’s a counterintuitive dynamic: the world’s largest producer is also deeply reliant on imports—not due to scarcity, but due to compatibility.

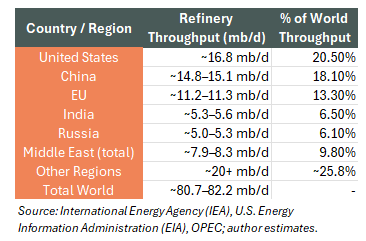

A Fragile Global System

Globally, refining capacity is highly concentrated. The U.S. and China together account for nearly 40% of refined fuel output. Add the EU, India, and Russia, and you reach roughly 65% of global capacity concentrated in just a handful of regions.

Now layer in geography and geopolitics.

Australia, for example, has minimal refining capacity and relies heavily on imports. That dependence becomes a vulnerability when global supply chains tighten—especially for diesel.

At the same time, global inventories of refined fuels are already low. Diesel reserves in particular are tight. Australia holds roughly a month’s worth of supply, while the U.S. maintains closer to four months. But even that buffer isn’t as comfortable as it sounds in a crisis.

The iesel Squeeze

The current pressure point in the system isn’t crude oil—it’s refined products, especially diesel.

Iran produces only a small share of global oil, but its broader region accounts for a significant portion of global supply. Any instability there risks disrupting flows through key chokepoints like the Strait of Hormuz.

Add sanctions on Russia, one of the world’s largest energy exporters, and the system tightens further. Diesel markets don’t have much slack to begin with, so removing even a portion of supply creates immediate strain.

This is why, despite political tensions, Russian oil has continued to find its way into global markets—through alternative routes, shadow fleets, and policy exceptions. There have even been periods where strategic decisions were made to allow limited flows simply to stabilise supply.

At one point, coordinated action from major economies saw hundreds of millions of barrels released from strategic reserves—the largest such intervention in history. Not as a long-term solution, but as a pressure valve to prevent a sharper economic shock.

Why It Matters More Today

It’s tempting to compare current tensions to past conflicts, like the tanker wars of the 1980s. But the global economy today is far more interconnected—and far more dependent on continuous energy flows.

Daily oil consumption is significantly higher. Supply chains are tighter. Inventories are leaner. There’s less room for error.

A disruption today doesn’t just affect fuel prices—it impacts food production, shipping costs, inflation, and ultimately economic growth.

The Bigger Picture

The global oil market isn’t just about supply and demand. It’s a high-stakes system shaped by chemistry, infrastructure, and geopolitics.

Chemistry determines what each barrel can produce

Infrastructure determines where it can be refined

Geography determines how it moves

Politics determines whether it flows at all

And sitting at the centre of it all is diesel—the fuel that quietly powers the real economy.

When that system is running smoothly, it’s invisible. When it breaks, everything feels it.