Mini Series: Arm to sell its own chips, eyeing sales goal of $15 billion

Arm’s Next Act: From Hidden Infrastructure to AI Powerhouse

One of the most important companies in the world isn’t a household name, but it powers nearly every device you use daily. That company is Arm Holdings.

For decades, Arm has operated behind the scenes, quietly becoming the architectural foundation of modern computing. But today, it’s making a strategic shift that could redefine its role in the semiconductor industry and significantly expand its economic potential.

The Business Model: A Toll Booth on Global Compute

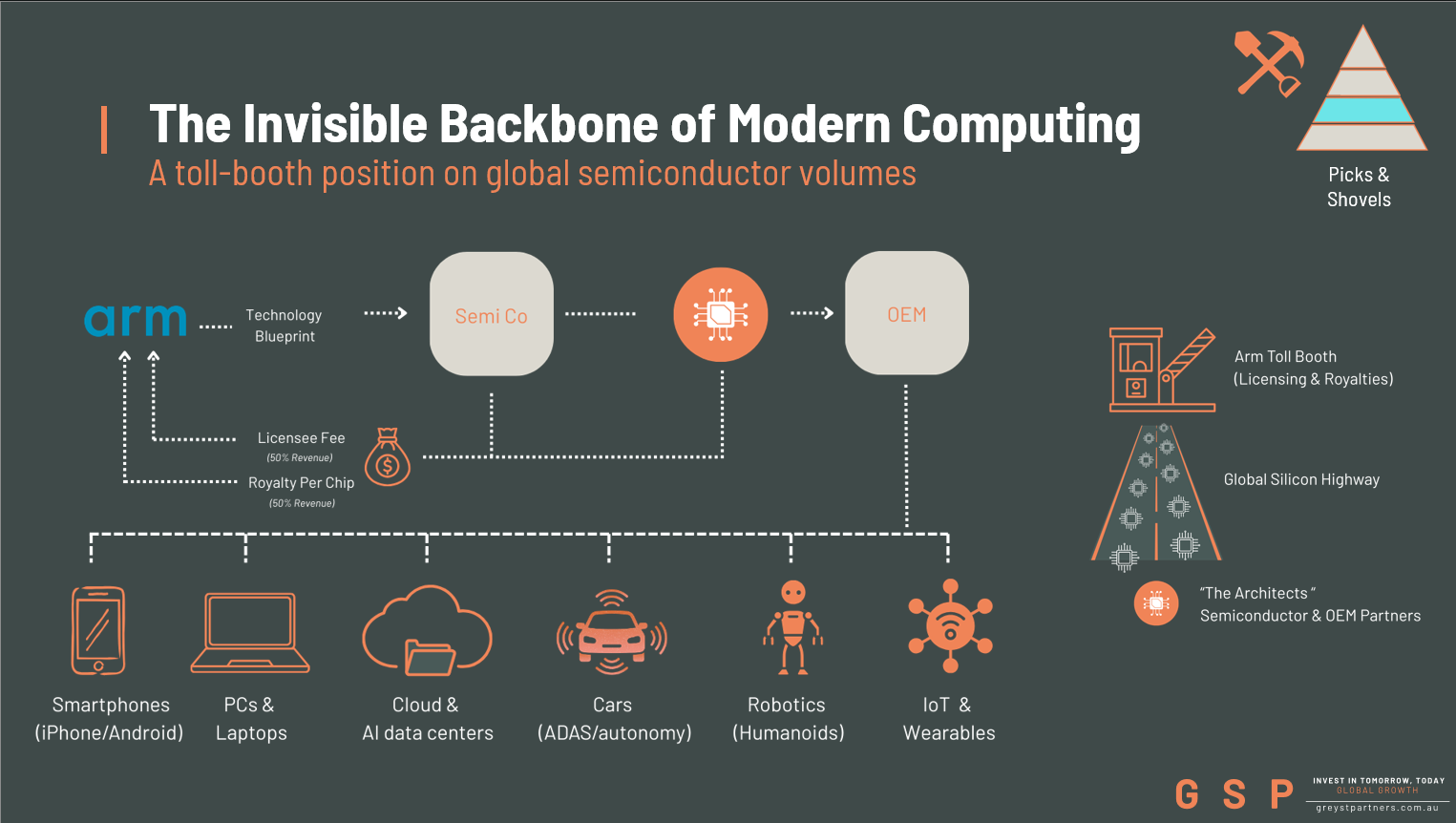

Arm is not a traditional chipmaker.

Instead, it designs the instruction set architecture (ISA) and CPU blueprints that semiconductor companies use to build processors. In simple terms, Arm creates the “language” that chips speak, and licenses it to companies like Apple, Qualcomm, and Samsung.

This model has two defining characteristics:

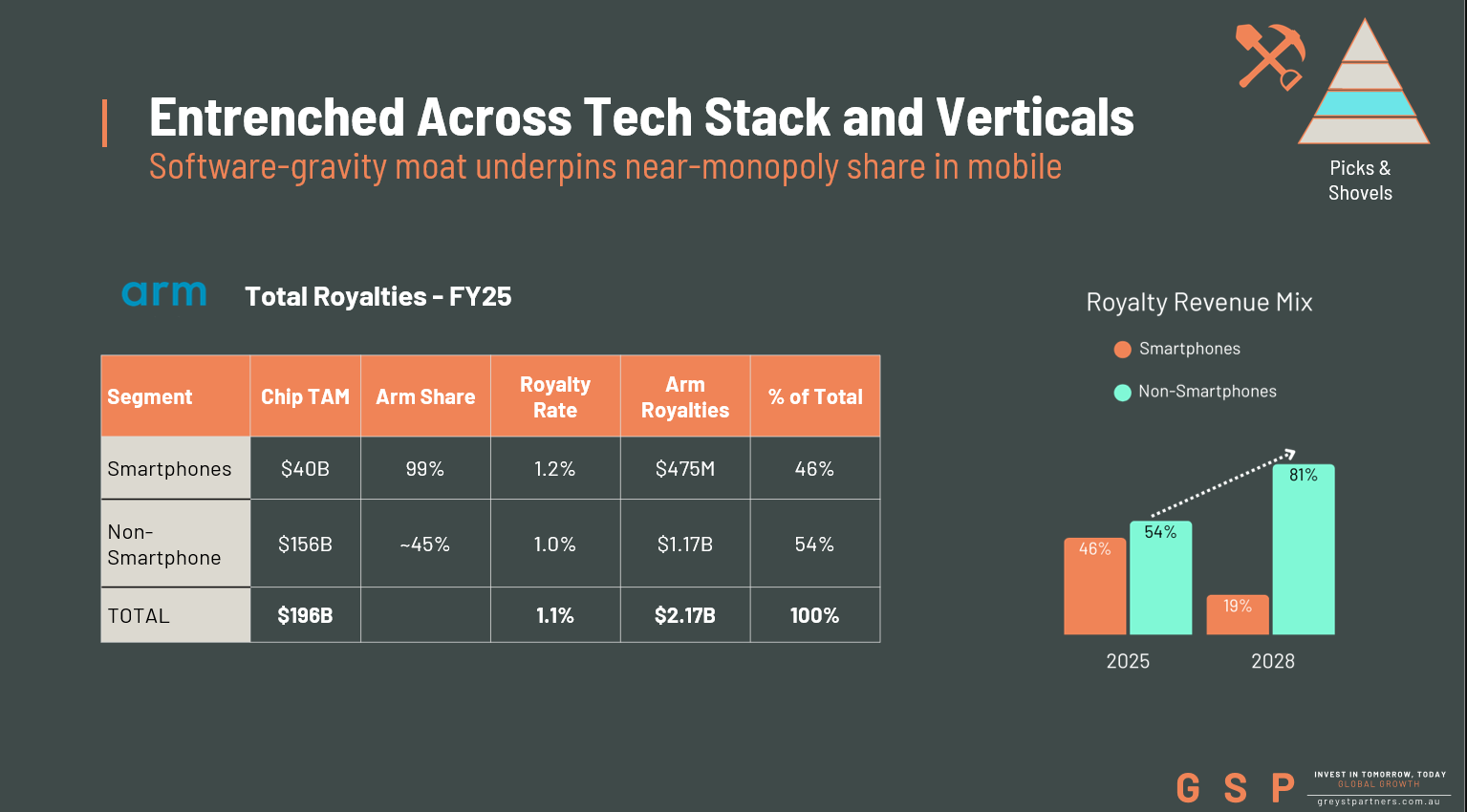

Scale: Arm-based chips are used in roughly 99% of the world’s smartphones, giving it near-total dominance in mobile compute.

Economics: Its licensing and royalty model is capital-light, generating ~97% gross margins and highly recurring, volume-linked revenue.

Every time a chip using Arm’s architecture ships, Arm earns a royalty. This creates a toll-booth position on global semiconductor volumes, largely insulated from manufacturing risks like foundry capex or inventory cycles.

The Moat: Software Gravity and Ecosystem Lock-In

Arm’s real advantage isn’t just its technology — it’s its ecosystem.

The ISA acts as the contract between software and hardware. Once developers, tools, and operating systems are built around it, switching becomes extremely difficult and costly.

This “software gravity” has entrenched Arm across multiple markets:

Mobile: ~99% share of application processors

Consumer electronics & IoT: strong and growing penetration

Cloud computing: increasing adoption via custom silicon

Automotive: deeply embedded in infotainment, ADAS, and autonomous systems

As a result, Arm is no longer just a mobile story — it’s becoming ubiquitous compute infrastructure.

The Strategic Shift: Moving Up the Stack

Historically, Arm has stayed out of manufacturing, focusing purely on IP.

That’s now changing.

Under CEO Rene Haas, Arm is moving into selling its own chips, starting with a high-performance processor designed for AI workloads — the Arm AGI CPU.

This chip reportedly features 136 cores, a massive leap compared to:

4–16 cores in typical consumer devices

~64 cores in high-end server CPUs

Meta Platforms is already an early customer.

This move marks a fundamental shift:

Arm is transitioning from a behind-the-scenes enabler to a direct participant in high-performance computing.

Why This Matters: A Step-Change in Revenue Potential

Arm’s traditional model has delivered consistent, high-margin growth — but it captures only a small portion of the total chip value.

By selling its own chips, Arm can move further up the value chain.

The potential impact is significant:

Management and analysts suggest chip revenue could reach ~$15 billion annually within five years

This could rival or even surpass Arm’s current licensing and royalty business

In other words, Arm is no longer just monetizing volume — it’s starting to monetize value.

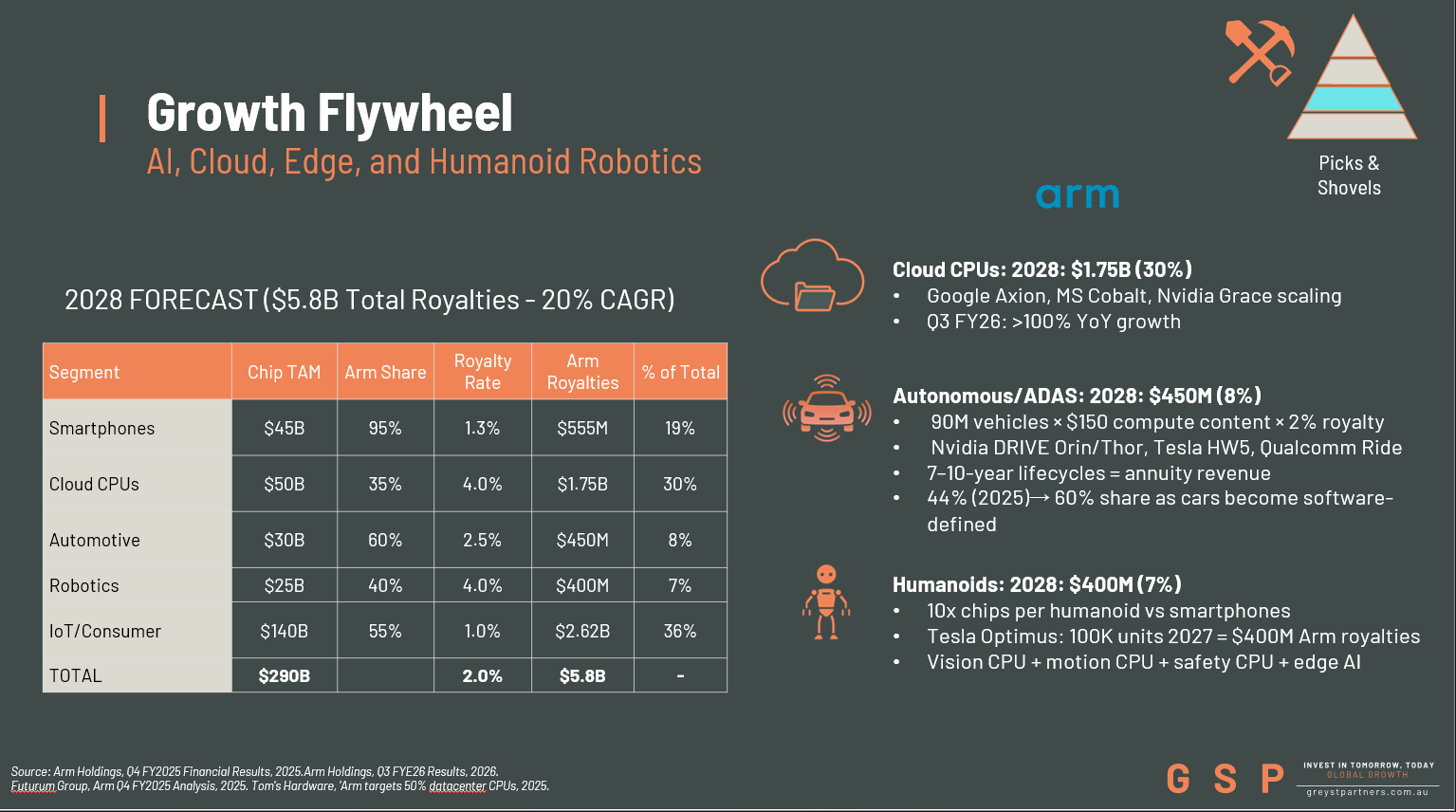

The Growth Flywheel: AI, Cloud, Autos, and Robotics

Arm’s long-term growth is being driven by a powerful multi-market flywheel:

1. Data Centers (Cloud CPUs)

Hyperscalers are increasingly designing custom Arm-based chips:

Amazon (Graviton)

Google (Axion)

Microsoft (Cobalt)

Nvidia (Grace)

Cloud CPU royalties are expected to grow from ~5% of total royalties today to ~30% by 2028, driven by performance-per-watt advantages and AI workload scaling.

2. Automotive and ADAS

Modern vehicles are becoming software-defined platforms.

Arm IP is embedded across:

Infotainment systems

ADAS (advanced driver-assistance systems)

Autonomous driving stacks

Crucially, automotive design cycles last 7–10 years, turning each design win into a long-duration royalty stream.

3. Edge AI and IoT

AI is moving beyond the data center to billions of edge devices:

Smartphones

Wearables

Industrial sensors

Smart infrastructure

Arm’s low-power architecture makes it the default choice for on-device AI inference, compounding volumes from an already dominant base.

4. Humanoid Robotics

An emerging but potentially massive opportunity.

Humanoid robots require multiple CPUs per system — for vision, motion planning, safety, and AI inference — often 10x the compute footprint of a smartphone.

Arm’s modular IP stack and energy efficiency position it as a natural architecture for this category as it scales.

The Big Picture: From Mobile Leader to AI Infrastructure

Arm is undergoing a transformation.

What began as a mobile-centric licensing business is evolving into a core infrastructure provider for the AI-driven economy.

It dominates smartphones

It’s scaling rapidly in data centers

It’s embedded in next-generation vehicles

And it’s positioned for emerging categories like robotics

At the same time, its move into chip manufacturing opens a new layer of monetization that could materially expand its revenue base.