Mini Series: The Most Irrational Trade in the Market Right Now

What Is the HALO Trade?

The HALO trade refers to investors paying a significant valuation premium for companies perceived as safe, dominant, and resilient.

HALO stands for Heavy Assets, Low Obsolescence — businesses with physical infrastructure, distribution networks, or entrenched brands that are unlikely to be disrupted by technologies like artificial intelligence.

Think large-scale retailers, consumer staples, or infrastructure businesses.

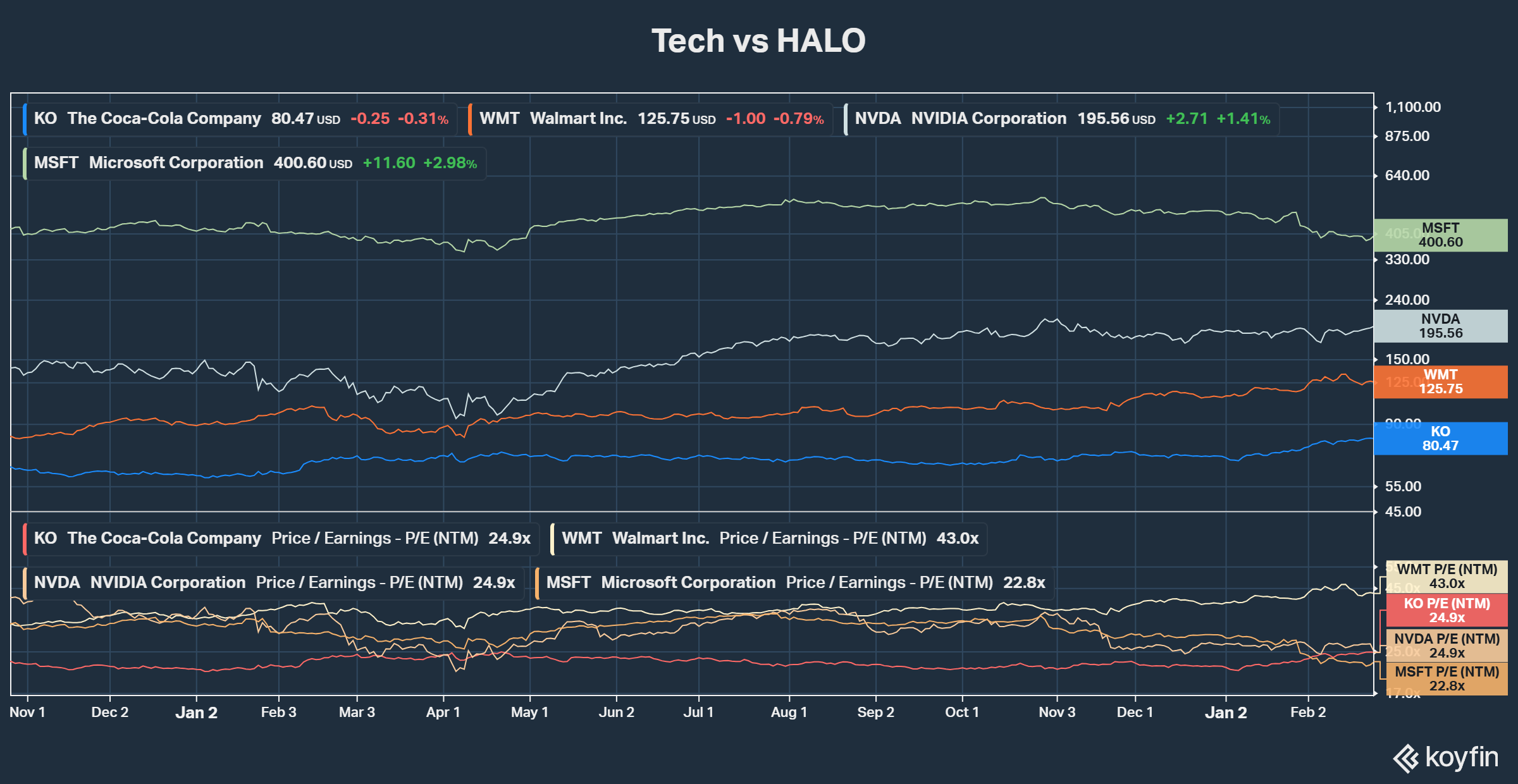

Companies such as Walmart and Coca-Cola fall into this category.

In an environment where investors are increasingly concerned about AI disruption, geopolitical risk, and economic uncertainty, capital has been flowing into these businesses because their earnings appear stable and predictable.

The logic is understandable.

But the valuation gap the trade has created is becoming difficult to justify.

Growth vs Valuation: The Gap Is Widening

Consider the following comparisons.

NVIDIA is currently trading at roughly 25× forward earnings (PE), with analysts expecting earnings per share growth of more than 37% annually over the next three years.

Similarly, Microsoft trades at around 23× forward earnings (PE), with expected earnings growth of roughly 18% per year.

These are companies sitting at the center of the AI infrastructure boom.

Meanwhile, several HALO trade beneficiaries are commanding far higher multiples despite far slower growth.

Walmart, for example, is trading closer to 43× forward earnings (PE), while expected earnings growth is roughly 10% annually.

Coca-Cola trades near 25× forward earnings (PE), with growth closer to 7%.

In other words, the market is assigning nearly a 2× valuation premium to companies with a fraction of the earnings growth.

This is not necessarily a criticism of these businesses. They are high-quality companies with strong brands, durable cash flows, and global scale.

But the pricing gap relative to growth fundamentals is becoming increasingly difficult to ignore.

Tech’s Rare Underperformance

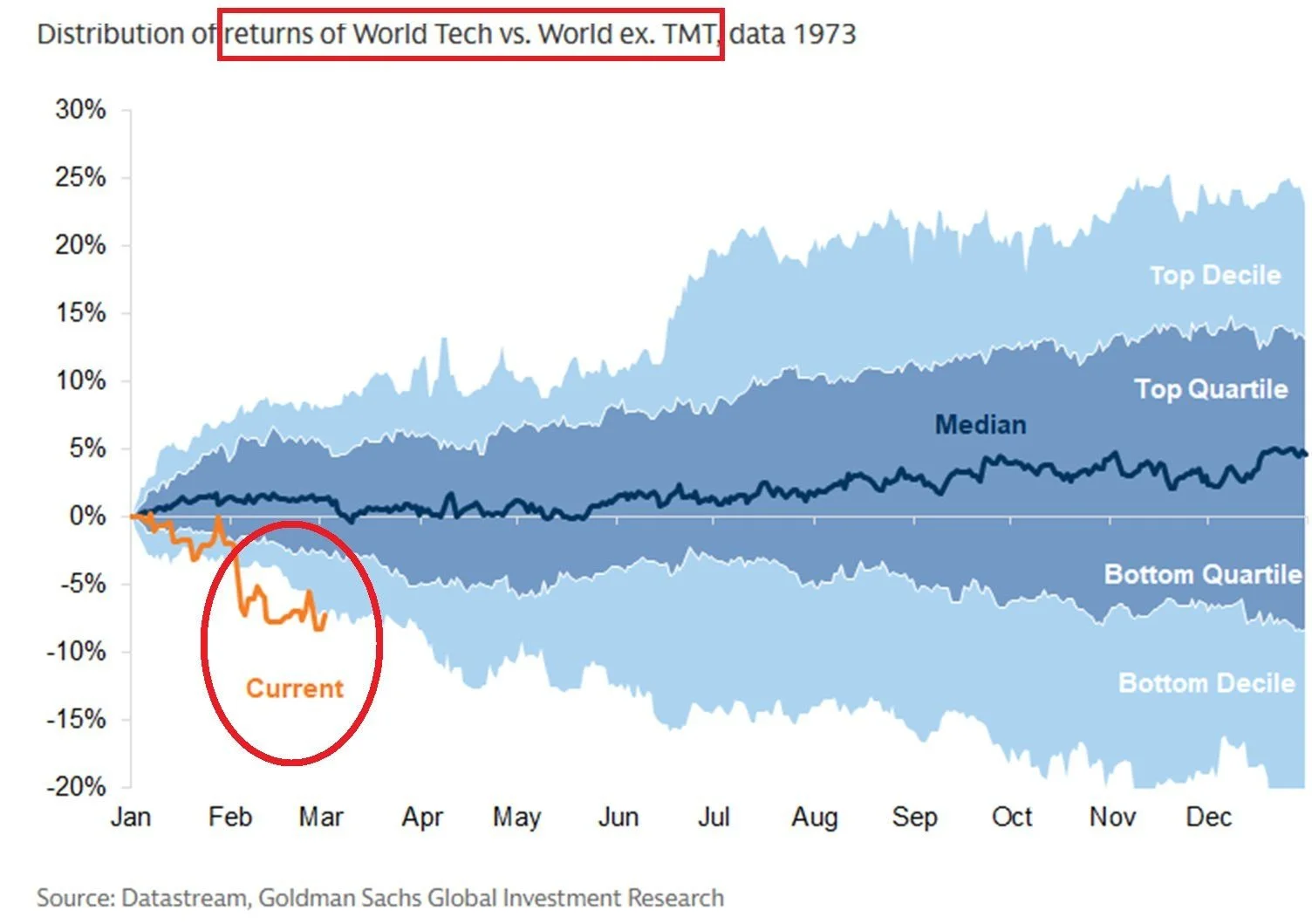

The rotation away from technology has also pushed the sector into historically rare territory. According to research from Goldman Sachs, global technology equities are currently underperforming the rest of the market by roughly 7 percentage points.

That places the sector in the bottom 10% of yearly starts going back to 1973.

Periods like this have historically been rare. More interestingly, history suggests the median outcome by year-end is roughly +4 percentage points of outperformance for technology stocks.

The last time technology underperformed this severely early in the year was around the Dot-com bubble era in the early 2000s. Of course, history does not repeat perfectly. But it often rhymes.

Earnings Momentum Is Still Strong

What makes the current sell-off particularly unusual is that technology earnings are not deteriorating.

In fact, they are accelerating.

Earnings growth across the S&P 500 Information Technology sector continues to trend higher, driven by strong demand for AI infrastructure, cloud computing, and semiconductor capacity.

Companies building the backbone of the AI economy — from data centers to advanced chips — are seeing rapid increases in revenue and profit growth.

Yet valuations across parts of the sector are compressing.

This creates a rare situation where earnings are rising while multiples are falling.

Historically, these types of dislocations tend not to persist indefinitely.

Why Investors Are Chasing Safety

The surge in the HALO trade reflects something deeper about investor psychology.

Periods of macro uncertainty often lead investors to prioritize:

Stability

Predictability

Resilient cash flows

Businesses with strong brands, entrenched distribution networks, and consistent demand often become perceived as safe havens.

But when too much capital crowds into the same defensive trades, valuations can stretch well beyond what underlying growth would justify.

And that appears to be happening now.

The Market’s Long-Term Rule

Markets can remain irrational for extended periods.

Narratives shift. Capital rotates. Risk appetites change.

But over long time horizons, equity markets tend to reconnect with a simple principle:

Earnings drive share prices.

Companies that consistently generate strong profit growth tend to create the most shareholder value over time.

Which raises an important question for investors today:

If growth remains strong in technology, and valuations continue to compress, how long can that divergence really last?