November Update

November 2026 has proven to be a very turbulent month for global equity markets, particularly US Tech Growth. From lofty peaks in late October, equities plunged sharply, marking one of the most notable drawdowns of the year. Investors faced heightened volatility, making this a month that will be remembered for both the speed and intensity of market swings.

Stay The Course - Pullbacks are normal and healthy

Volatility is all part of investing in the equity market. But this year is an anomaly, we saw rapid drawdowns in February and March, and then a major April drawdown, followed by a sharp rally into October. Markets were due for a healthy pullback and we got it.

If you want the magic of compounding that has delivered ~10% annualized returns in the S&P 500 since 1936, you have to sit through the turbulence:

• 3 corrections of 5% per year

• 1 correction of 10% per year

• 1 correction of >15% once every 3 years

• 1 correction of >20% once every 6 years

These aren’t anomalies, they’re the historical norm. The market doesn’t go up in a straight line; it climbs a wall of worry.

Long-term wealth isn’t built by avoiding volatility, it’s earned by staying invested through it. Volatility is the price of admission for superior returns. Pay it gladly, or settle for cash under the mattress.

| S&P 500 YTD Performance (till 21st Nov) | Contribution |

|---|---|

| Total SPX YTD Gain | 19.4% |

| 20% | |

| Broadcom | 8% |

| Nvidia | 16% |

| Microsoft | 6% |

| Total from these stocks | 50% |

Why We Could See a Push Higher Into Year-End

There are a few reasons as to why markets could push higher into years end.

1. US Government Shutdown is OVER

43-day shutdown (longest ever) ended mid-November

Removed massive uncertainty + cleared the backlog of economic data

Markets hate uncertainty — now it’s gone → green light for risk-on

2. December Rate Cut is Basically a Done Deal

CME FedWatch now showing 83% chance of a 25 bps cut on Dec 18

Just a month ago it crashed from 90% to 30% because of shutdown noise → now back above 80%

The data never changed: September CPI showed clear deflation in the big components, labor market softening, air traffic collapsing during shutdown → no immediate inflation threat

Bottom line: the cut was always coming — the market just got scared for a minute

3. This is the “All-Clear” Signal from the Fed

We’ve now had two cuts (Sept + Oct) → a third in December ends the Fed’s “extended pause”

Exact playbook we saw in 1998 and 2024 — both times the Fed did three cuts in four months and the S&P ripped into year-end

More liquidity, no recession = rally fuel

4. Markets Got Way Too Oversold

Mid November the S&P RSI dropped to ~35 — classic oversold

Huge sideline cash + heavy short covering → perfect “buy-the-dip” setup that we’re already seeing play out.

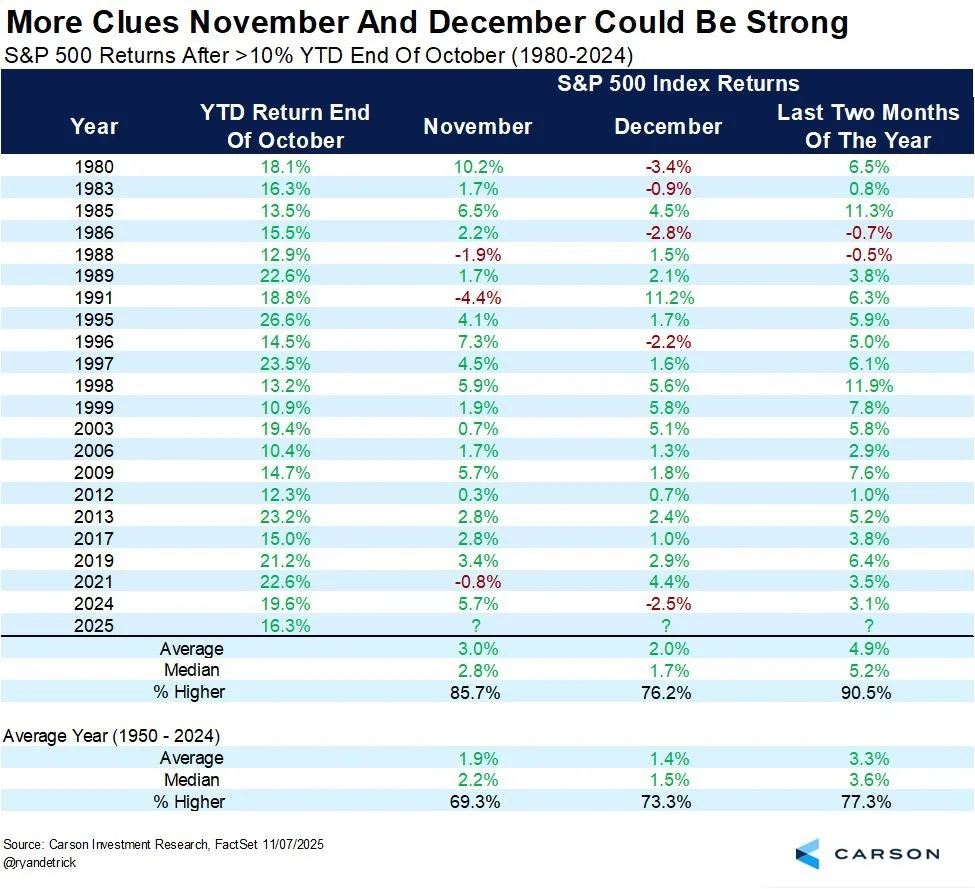

5. Seasonality is Rocket Fuel Right Now

Since 1950, when the S&P is already up 10%+ through October, Nov + Dec have averaged +3.3%

Since 1980 (more relevant today) → +4.9% average

The Big Picture: Volatility is back, and with it, both risk and opportunity

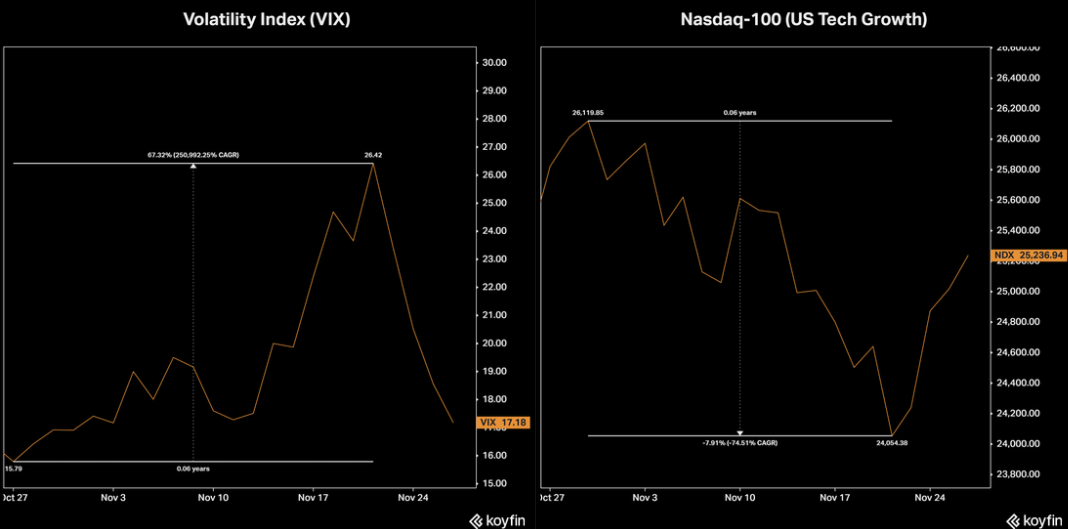

Global equities experienced a sharp pullback this month. The S&P 500 fell roughly -5.8% from its late-October peak, while the tech-heavy Nasdaq-100 dropped -8.6%, with growth-focused indices taking the hardest hit. Similar declines were seen across major markets in Europe and Asia, as investors quickly reassessed risk and adjusted their portfolios.

After a prolonged period of unusually low volatility, market swings surged dramatically. The rapid shifts served as a stark reminder that even during extended periods of calm, sentiment can turn quickly, triggering swift and pronounced reversals.

The November pullback has sparked a debate: is this a “speed bump” or the start of a broader correction? Some strategists see this as a temporary pause, with valuations resetting before a potential rebound.

Why the drawdown and volatility?

The volatility erupted when a brutal bond-market sell-off blindsided investors. A surprise hot November jobs print (+258k) and sticky core PCE shredded the “December cut is locked” narrative overnight. Fed pricing flipped violently, terminal rate expectations lurched from 3.25% to 3.75% in days, 10-year yields spiked 38 bps in a week, the VIX rocketed from 14 to 34, and long-duration growth names got torched on the higher discount rates.

At the exact same moment, bears weaponised “AI ROI anxiety” headlines as big tech names like Meta, Google, Microsoft and Amazon had just raised 2026 capex guidance again.

The two triggers fed a perfect de-risking storm.

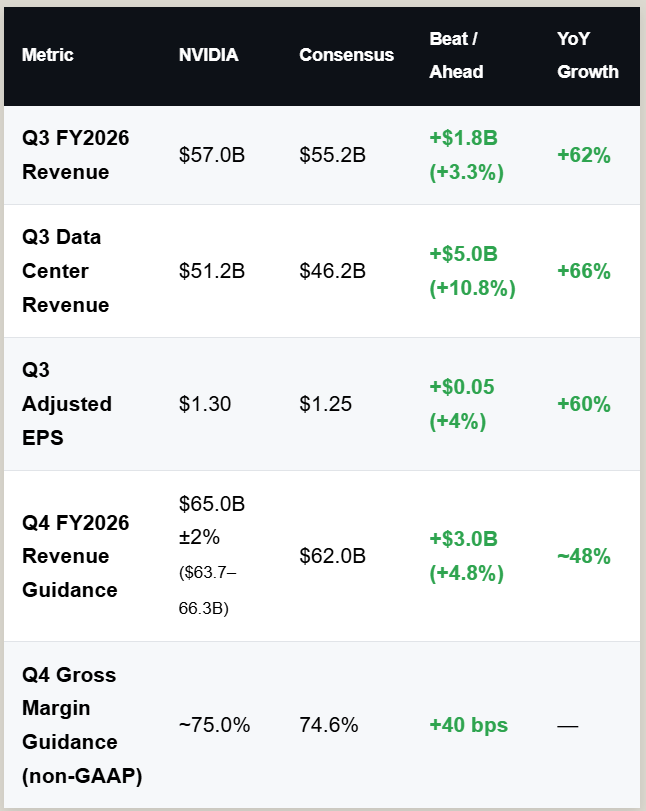

NVDA Monster Print

NVIDIA absolutely crushed its Q3 earnings. Revenue hit $57 billion, easily beating the $55 billion consensus. Adjusted EPS came in at $1.30, topping the $1.25 estimate. Data Center revenue soared to a record $51.2 billion. This was not a surprise to anyone paying attention, but guidance ahead was the big risk factor and they delivered.

The biggest risk heading into the print was forward guidance, and NVIDIA delivered in a massive way. They guided Q4 revenue to as high as $66 billion, representing roughly 50% year-over-year growth and blowing past the $62 billion Wall Street was looking for.

Jensen Huang went further on the call: NVIDIA already has half a trillion dollars ($500 billion) in AI chip orders locked in for 2025 and 2026. Every single cloud GPU is sold out, even the older A100 generation is completely booked for months. According to Wedbush’s Dan Ives, widely regarded as the top tech analyst on the Street, demand for NVIDIA GPUs is running at a staggering 10 to 1 ratio. For every chip they can ship, ten customers are ready to buy.

The bears who spent weeks calling this a bubble and demanding a “show me” quarter have gone completely silent and retreated back into hibernation. This print and guidance confirmed the AI spending boom is not only real, it is accelerating.

NVIDIA remains the undisputed king of the AI era,.

US Fed Rate Cut Likely Done Deal

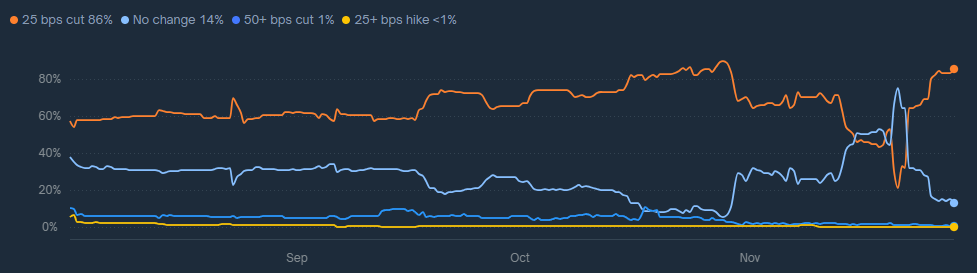

Prediction markets like Polymarket offer a raw, crowd-sourced pulse on Fed expectations. For the December 2025 FOMC meeting, the "25 bps cut" probability (to 4.25-4.50%) started late October at a frothy 90%, riding post-September/October easing highs and soft CPI prints. But mid-November's hot jobs data (+258k) and sticky core PCE flipped the script, cratering odds to a gut-wrenching 22% by November 20 as inflation fears peaked. Traders piled into hold bets, amplifying the de-risking storm.

Fast-forward to November 27: Odds have roared back above 80% (86% on Polymarket), fueled by dovish NY Fed comments, a cooling 2.6% core PCE, and rebounding risk appetite. This echoes 1998/2024's three-cut sequences, where a third trim ignited 15%+ S&P rallies sans recession signals. Polymarket's rebound screams "all-clear" liquidity unlock could supercharge year-end rally, this pivot greenlights Santa Rally potential.

Polymarket - What will the Fed do at the upcoming meetings?