In The Press: Ausbiz - Are markets mispricing this social media giant?

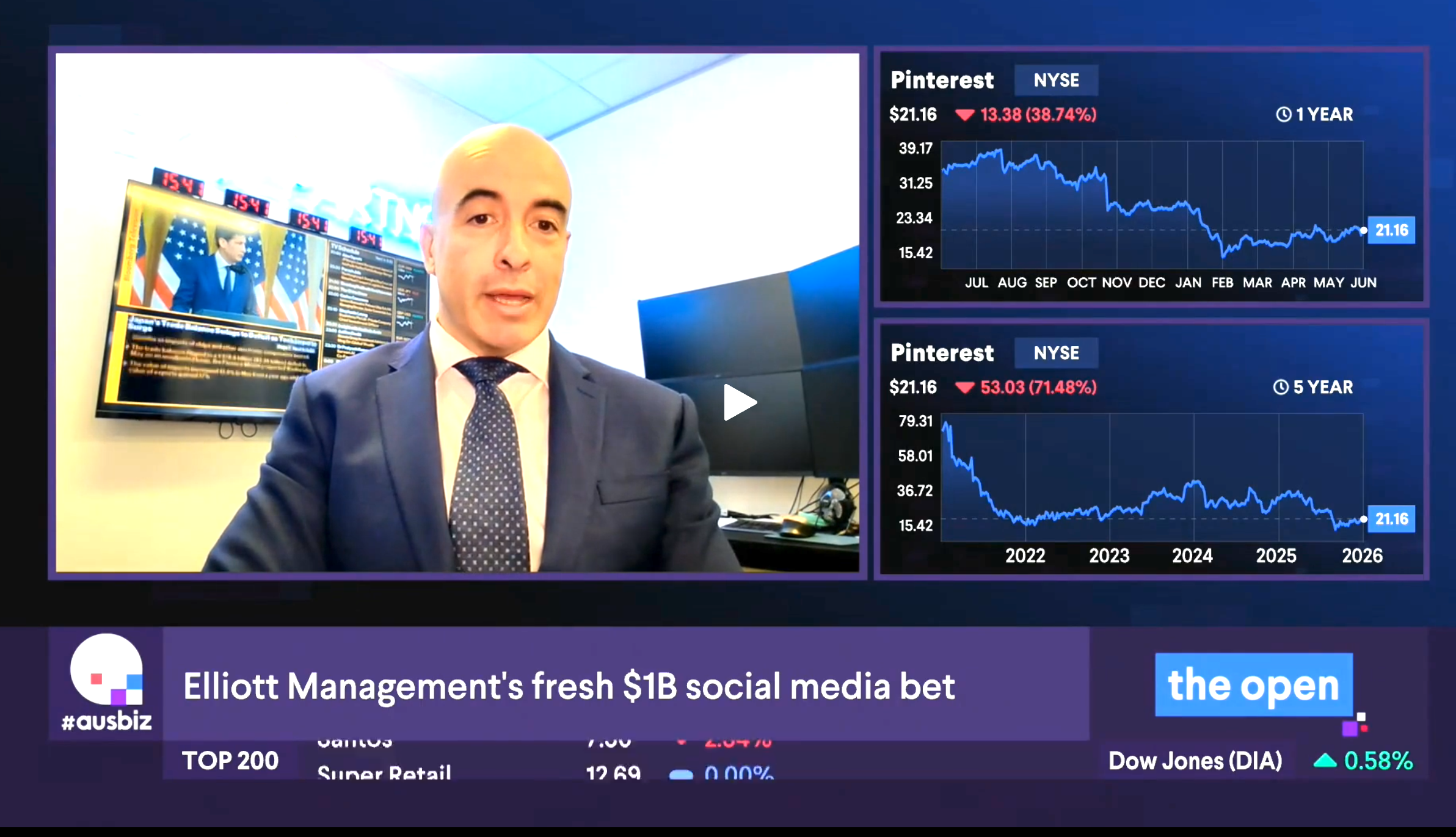

Huw Davies, Founding Partner and Portfolio Manager, spoke on Ausbiz to discuss Elliott Management’s ~10% stake in Pinterest. He views the activist investor’s $1 billion commitment as a high-conviction bet on under-monetised scale in an already successful platform, rather than a distressed turnaround. Pinterest delivers 18% YoY revenue growth to over US$4 billion annualised, with 631 million MAU and strong free cash flow. Yet the market prices it as a second-tier social stock. Davies sees it as a high-intent discovery and commerce platform, with Meta’s AI-powered monetisation as the blueprint Elliott will likely push Pinterest to follow for significant earnings upside.

Watch Here: Are markets mispricing this social media giant?

Elliott Management’s $1 Billion Bet

Most investors see Pinterest as a second-tier social media company. I think that’s the wrong framework.

It’s more of a discovery platform where people go to plan purchases. They are looking for fashion, home renovations, travel ideas, weddings, beauty products and retail purchases. That’s very different behaviour from scrolling Instagram or TikTok.

The investment opportunity is that Pinterest has already achieved enormous scale, but it still monetises that user base far less effectively than Meta.

The Numbers Tell a Different Story

Let’s start with what Pinterest actually delivered last quarter.

Revenue grew 18% year-on-year to just over US$1 billion. Monthly active users grew 11% to 631 million. Free cash flow was US$312 million.

This isn’t a turnaround story. This isn’t a distressed asset. It’s a business generating over US$4 billion in annualised revenue, growing at double digits and producing significant cash flow.

The Market Is Focused on the Wrong Problem

The share price over the past 12 months has reflected advertising cyclicality, competition concerns, and prior guidance disappointments.

What investors are missing is that Pinterest doesn’t have a user problem — it has a monetisation problem. And those are very different things.

The question isn’t whether Pinterest has value. The question is whether management can capture more of that value.

Elliott’s Real Thesis

I don’t think Elliott sees a social media company. I think they see a commerce and discovery platform.

Pinterest users arrive with intent, they aren’t killing time. They’re planning purchases, researching products and discovering brands. That behaviour is extremely valuable.

The challenge is that Pinterest still earns significantly less revenue per user than platforms like Meta.

Meta Is the Blueprint

This is where Meta becomes the comparison.

Meta’s latest quarter was extraordinary:

Revenue grew 33% to US$56.3 billion

Ad impressions increased 19%

Price per ad increased 12%

Operating margins exceeded 40%

Meta has shown what happens when AI, advertising and monetisation all work together.

The reason we own Meta is because it’s already proven this model works. The reason we bought Pinterest is because it hasn’t — yet.

The Monetisation Gap Is the Opportunity

Pinterest generated roughly US$1.61 revenue per user last quarter. Meta generated over US$13.

The gap is massive, yet Pinterest users often show stronger commercial intent. Someone on Pinterest isn’t casually browsing — they’re planning a kitchen renovation or shopping for a wedding.

Elliott will push management to close this gap through higher ad-load efficiency, better conversion, and stronger retail media monetisation. International expansion is a particularly large lever: Europe and Rest of World together represent hundreds of millions of users but currently deliver far lower ARPU than the US.

Even moving global ARPU from ~$1.60 toward $2.50–$3.00 would create enormous earnings leverage at 631 million users.

AI + Buyback = Earnings Acceleration

Pinterest’s AI strategy is built for exactly this: visual search, personalised discovery, generative tools for advertisers, and cost-efficient open-source models. Because the platform is image-first and commerce-linked, AI improvements flow directly to relevance, targeting, and conversion.

The US$3.5 billion buyback (around 30% of market cap at announcement) plus earlier restructuring adds capital discipline and EPS leverage on top of any operating improvement.

Success doesn’t require Pinterest to become Meta. It just requires it to become a better, more monetised version of itself — continued user growth, international ARPU lift, AI-driven conversion gains, and aggressive capital return.

When earnings grow meaningfully faster than revenue, multiples tend to expand.