June Update

June was marked by elevated volatility and clear theme consolidation across markets. Best performing US Sectors were Industrials, Health Care and Financials. The S&P 500 finished down -1.32% for the month. The US dollar appreciated on the back of rising Treasury yields and growing speculation around potential Federal Reserve rate hikes under the new Fed Chair, following Hawkish tone, however, at the later stages of the month Inflation expectations fell sharply. These macro cross-currents amplified rotations within technology and added pressure on rate-sensitive areas. Meanwhile, progress in Iran-US peace talks contributed to lower oil prices and a decline in gold, suggesting markets are pricing in reduced geopolitical risk yet the inflation backdrop remains concerning due to persistently elevated fertilizer costs and food security risks.

Check-Writers vs Check-Receivers

The market drew a sharp distinction between those writing the checks (hyperscalers funding record AI infrastructure spend) and those receiving the checks (semiconductors, especially memory and AI-related names).

The Goldman Sachs baskets illustrate the divergence clearly:

GS US AI Semis (Check-Receivers) extended gains, recently reaching 271.81.

GS US Hyperscalers (Check-Writers) peaked in mid-May before rolling over sharply to close the period at 96.29.

This reflects rising investor scepticism that the hyperscalers’ massive AI capex will deliver adequate near-term returns, even as the companies supplying critical components continue to benefit. Apple’s MacBook and Microsoft’s Xbox price increases are the first visible signs that these costs are reaching consumers.

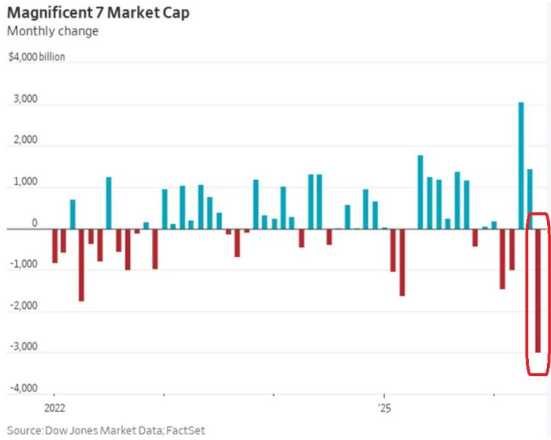

Magnificent 7: Record Destruction and the Capex Question

The Mag 7 erased nearly $3 trillion in market value in June, on track to be their worst month on record. The Roundhill Magnificent Seven ETF (MAGS) fell -12.9% month-to-date.

This was a targeted rotation, not a broad tech sell-off. Investors are no longer granting blanket permission for “AI spend at any cost.” While long-term free-cash-flow estimates for Alphabet, Meta, Microsoft and Amazon remain strongly upward through 2030, the near-term risk centres on timing and digestion of the capex cycle.

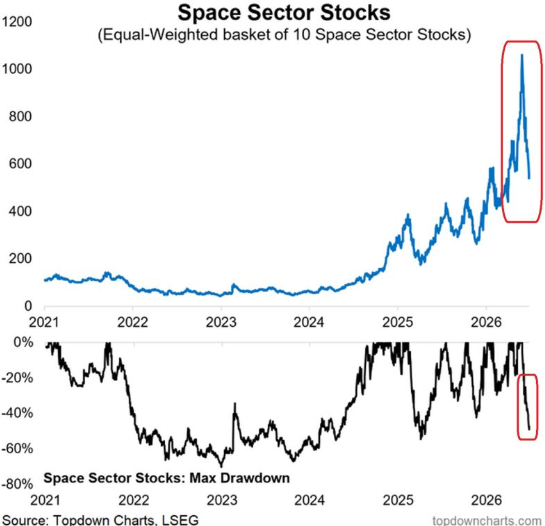

Space Sector: Stairs Up, Elevator Down

The space sector delivered one of the clearest examples of “stairs up, elevator down” in June. An equal-weighted basket of 10 space sector stocks collapsed approximately 50% from its peak, the largest drawdown since April 2025 and the second-largest since the 2022 bear market.

SpaceX shares ($SPCX) fell 32% from their mid-June peak following the June 12 IPO. Retail investors poured in aggressively, purchasing a record $405 million of shares in the first five trading days the largest first-week retail inflow for any IPO in history. They also piled into the 2x Leveraged Long SpaceX ETF ($SPCH), buying $65.8 million in its first few sessions. That leveraged vehicle subsequently dropped 56% from its peak on just the second trading day after launch. This rapid reversal highlights how quickly sentiment can shift once initial hype fades, even in structural themes.

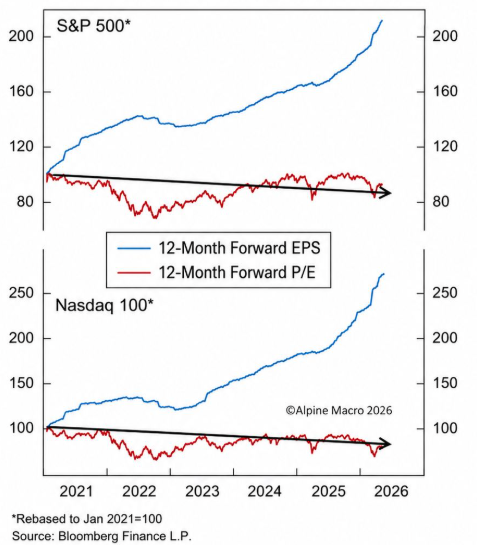

Valuations: The Bubble Is in the Denominator

Since January 2021, forward P/E ratios for both the S&P 500 and Nasdaq 100 have been flat to slightly down. There has been no multiple expansion, the usual late-cycle culprit simply never appeared. All of the market’s gains have instead come from rising 12-month forward EPS estimates, with the Nasdaq’s earnings line moving almost vertically higher. The market does not look expensive because investors are swallowing ever-higher projected profits without much questioning. That comfort is entirely borrowed from optimism around margins, AI capex productivity, and sustained growth delivery.

The real risk sits in the denominator. If forward earnings disappoint whether due to slower monetisation of AI investments, capex fatigue among hyperscalers, or broader macro pressure it will not be the multiple that absorbs the shock. The floor of the story will give way. In this environment, the most important thing to watch is not today’s P/E, but whether the aggressive earnings forecasts that have supported valuations can actually be delivered.

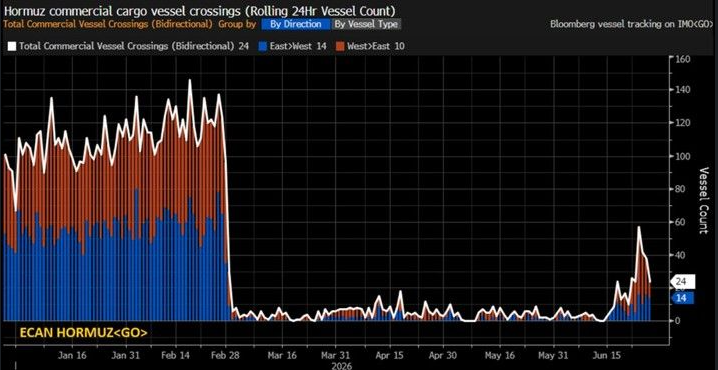

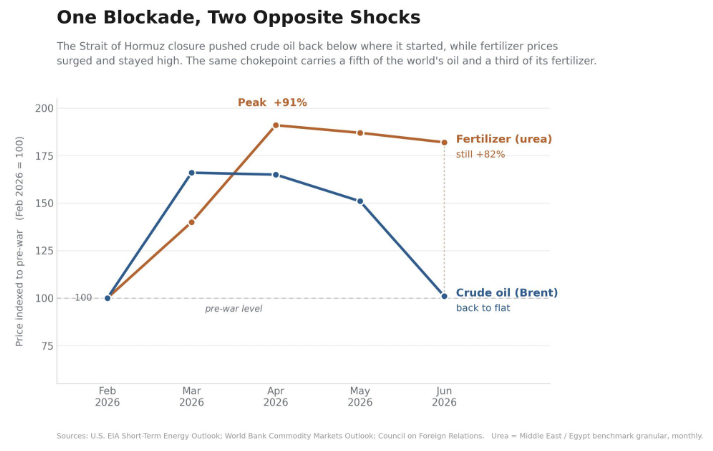

Pick up, Put Down. Traffic in the Strait of Hormuz

Recent developments suggest the situation remains fragile. Vessel traffic through the Strait has pulled back again, with crossings falling to just 24. This decline reflects renewed escalation after the U.S. conducted fresh strikes on Iranian targets around the Strait of Hormuz in response to a drone attack on the tanker M/T Kiku, days after an Iranian drone struck the container ship Ever Lovely, the first vessel hit since the U.S.–Iran ceasefire was signed. This back-and-forth is undermining efforts to restore normal marine traffic, with CENTCOM noting that commercial vessels are still transiting the Strait but at volumes well below pre-crisis levels.

Geopolitical De-escalation and Persistent Inflation Risks

Progress in Iran-US peace talks has allowed oil prices to fall back below $70, while gold has also retreated as the geopolitical risk premium fades. Markets are clearly pricing in reduced near-term conflict risk. However, the more important signal may be coming from fertilizer. Urea prices remain +82% above pre-crisis levels, with one-third of global traded fertilizer still moving through the Strait of Hormuz. Unlike oil, countries do not hold strategic fertilizer reserves. The biggest economies can absorb or substitute, but poorer, import-dependent nations cannot. This raises the risk of a more durable food security shock that could outlast the immediate energy market volatility, with second-order effects on global inflation and risk sentiment. Commercial vessel traffic remains well below pre-crisis levels.

New Fed Chair: Hawkish or Dovish?

Kevin Warsh took over and held his first FOMC meeting in mid-June 2026 (rates held steady at 3.5–3.75%). He delivered a notably hawkish message:

The Fed still released the SEP/dot plot on June 17.

It showed a clear hawkish shift from the other participants (the median for end-2026 moved higher, now pointing to a rate hike rather than a cut, with 9 of the 18 dots in or above the current range).

Emphasis on persistent inflation (still elevated, partly from the prior energy shock and other factors) and the Fed's commitment to price stability.

In his first FOMC meeting as Chair, Kevin Warsh made it clear that inflation remains too high and the Federal Reserve’s job is to bring it back to 2%. At the same time, he is deliberately stepping back from the heavy forward guidance and detailed rate projections that defined the Powell era. He wants a quieter, more disciplined central bank that focuses on what it does rather than constantly telling markets what it might do next.

| Theme | Warsh’s Position | Implication |

|---|---|---|

| Inflation | Still too high. The Fed will deliver price stability. “The recent past need not be prologue.” | Hawkish bias. No rush to cut rates. |

| Forward Guidance | Stripped most predictive language from the statement. Less signaling. | Harder for markets to front-run the Fed. |

| Dot Plot / SEP | Personally refused to submit a dot. Called the current format unhelpful. Launched a review. | Big signal the dot plot may be de-emphasized or changed. |

| Communication Style | Wants simpler, less frequent, less market-moving communication. | Moving away from the “Fed as oracle” model. |

| Institutional Reform | Announced multiple task forces to review communications, balance sheet, data, and inflation framework. | Positioning himself as a reformer. |

| Overall Philosophy | The Fed has become too big and too influential in markets. It should have a smaller footprint. | Less pre-commitment = more flexibility for the Fed. |

Inflation Expectation Down?

This dramatic move is largely technical/reversionary after an oil/geopolitical spike and unwind, classic behavior for a 1-year measure. It does not signal that inflation is suddenly crashing to 1% sustainably or that the Fed is about to pivot dovish. Core inflation remains above target, shelter is sticky, and tariffs/fiscal effects are still in play for later in 2026. The hawkish new Fed leadership under Warsh is focused on the persistent components and maintaining credibility. The market is simply pricing the transitory part of the recent inflation surge as fading fast due to cheaper energy. Longer-term inflation expectations remain far more contained around 2.2–2.5%. This is a classic example of how headline/transitory shocks can dominate short-horizon market measures while the underlying policy and structural picture evolves more slowly.