May Update

May delivered the best monthly return for our flagship GSP Global Growth Fund since launch, with gains of just over 11% (net) driven by the continuing AI infrastructure buildout and a swift recovery across software and cybersecurity. The AI trade has moved decisively beyond headline hype into identifiable supply chain bottlenecks, a shift that rewarded selective positioning.

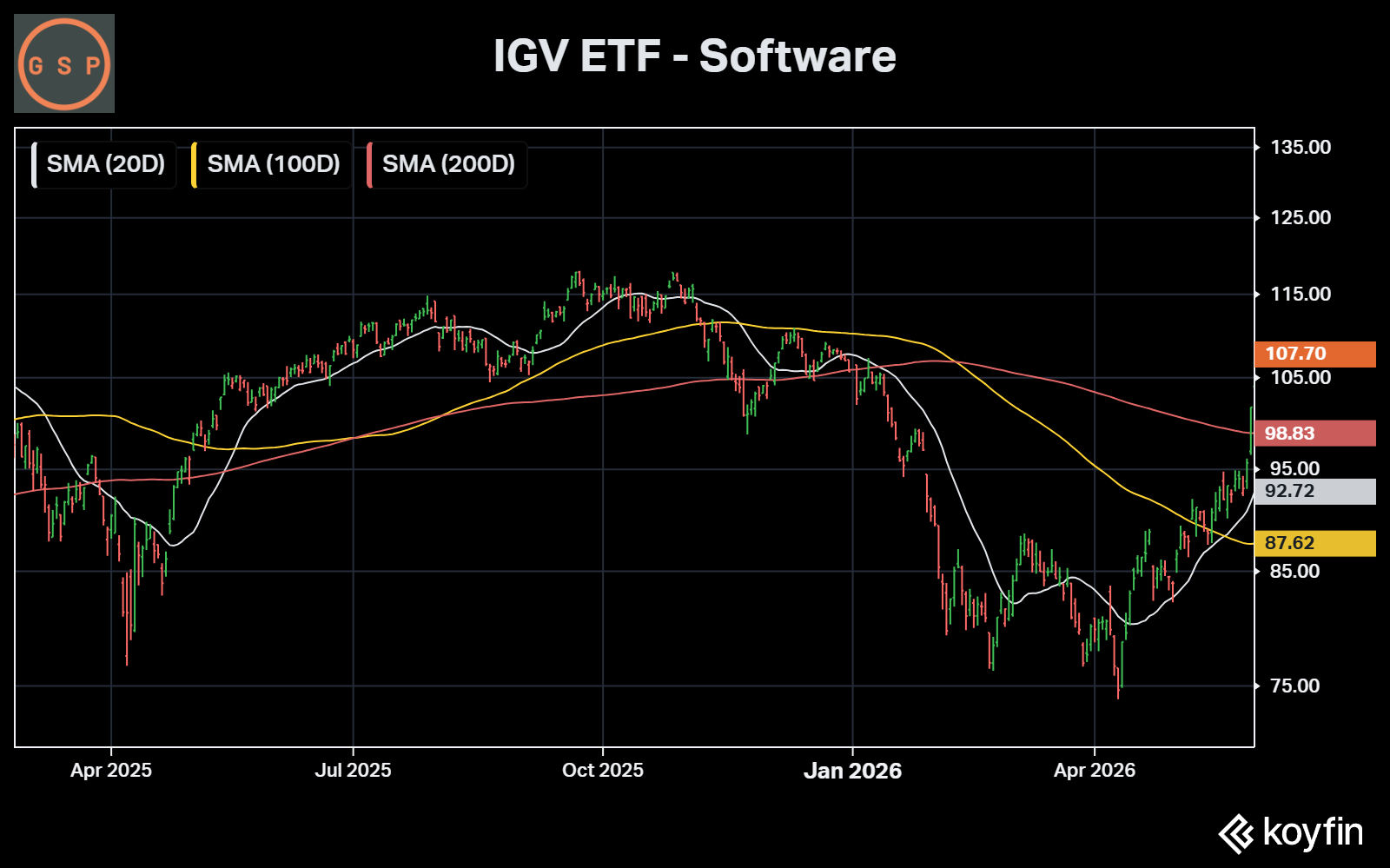

Software Sector Recovery & Usage-Based Pricing

Software participated meaningfully in the recovery. The iShares Expanded Tech Software Sector ETF delivered robust gains and attracted meaningful inflows as investor sentiment improved. A key structural driver is the ongoing shift toward usage-based consumption pricing models.

ServiceNow (NOW) reported that approximately 50% of its net new business in the most recent quarter came through usage-based models. This matters because agentic AI is increasingly taking over tasks previously performed by human workers, creating a gradual headwind for traditional seat-based licensing. Usage-based models scale with the volume of activity and workflows executed, including those driven by AI agents, providing a natural offset and expanding the monetisation opportunity as overall system utilisation rises.

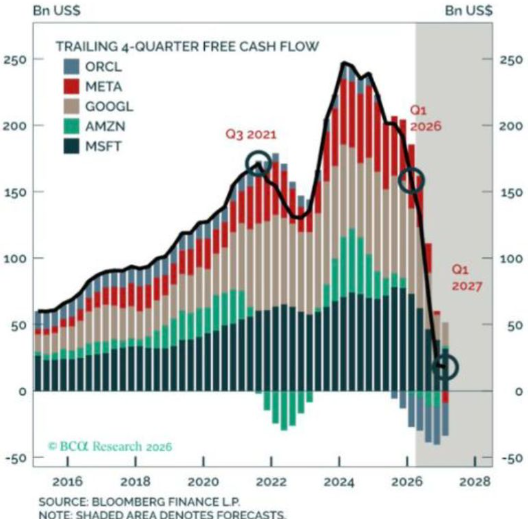

US Earnings Season & Hyperscaler CapEx Acceleration

The broader US earnings season delivered a strong beat rate across the S&P 500. The defining feature, however, was the continued acceleration in AI infrastructure spending by the major hyperscalers. Microsoft, Amazon, Alphabet and Meta all reported robust results, with cloud revenue growth remaining solid and AI-related demand accelerating across both training and inference workloads.

Collectively, the four hyperscalers guided for approximately $725 billion in combined capital expenditure for 2026. This represents a very large increase from the prior year’s roughly $410 billion, an uplift of around $315 billion or +77% year-on-year. The overwhelming majority of this incremental CapEx is directed toward AI hardware. This guidance confirms that the infrastructure buildout remains in its early stages.

AI Infrastructure Buildout: Memory, Custom Silicon & Supply Chain Winners

At the portfolio level, three positions captured the sharpest upside as the market moved beyond broad AI hype into specific supply chain bottlenecks: Arm Holdings, Advanced Micro Devices, and Micron Technology.

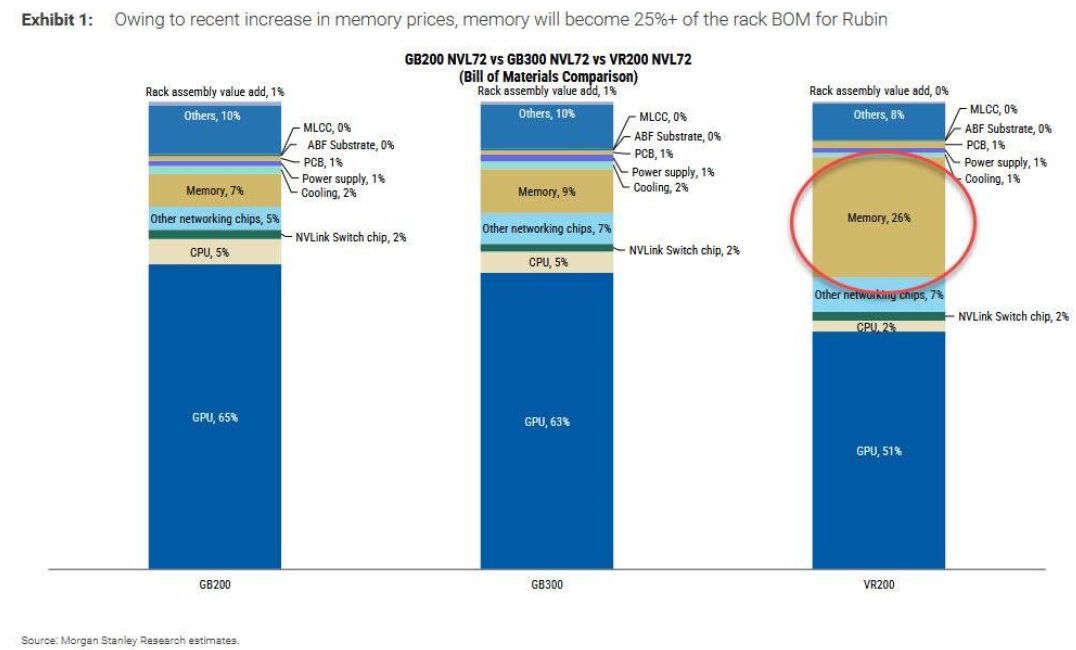

Memory: Rising Share of Rack BOM

Owing to recent increases in memory prices, memory is projected to become 25%+ of the rack Bill of Materials for next-generation Rubin systems (VR200 NVL72). This compares to approximately 7% in GB200 NVL72 and 9% in GB300 NVL72 configurations. The shift underscores the pricing power and strategic importance of high-bandwidth memory in the AI stack.

Micron Technology (MU)

Micron is a clear winner from the HBM bottleneck. AI workloads are driving elevated utilisation and pricing power. Structural supply growth of only around 20% per annum against much stronger data centre demand has left the three major memory makers controlling approximately 90% of the HBM market.

Arm Holdings (ARM)

Arm’s capital-light licensing model continues to scale as every major AI accelerator and custom chip generates royalty revenue. Its architecture is becoming the default for power-efficient custom silicon. Near-total dominance in smartphones, combined with a strong positioning in humanoid robotics (which require an estimated ten times the chip content of a flagship phone), provides additional long-term growth drivers.

Advanced Micro Devices (AMD)

AMD gained meaningful share in AI GPUs through the MI300 series on the back of strong performance per watt and an open software ecosystem. The company is establishing itself as a credible second supplier in a market that benefits from supply diversification.

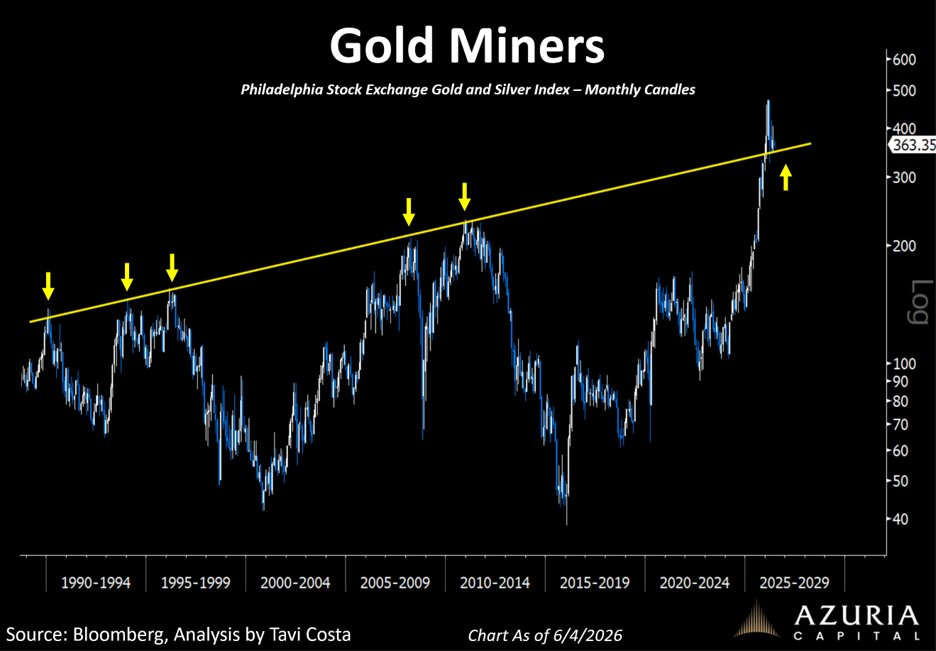

Gold: At the 200-Day Moving Average Amid Sentiment Reset

Gold prices broke below their 200-day moving average. The last time we were at these levels proved to be a constructive entry point for the asset class. However, we try not to get too fixated on technical levels alone. What stands out more is how dramatically sentiment has shifted. Just a few months ago, gold was one of the market’s favourite trades. Today, it feels almost completely forgotten.

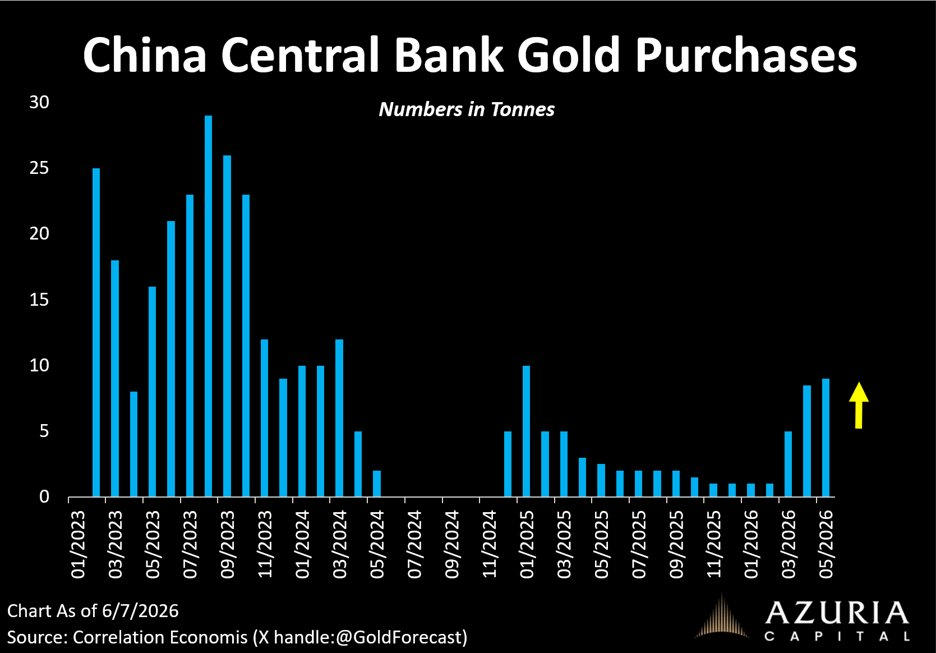

China’s gold buying spree continues unabated. The metal is steadily moving from weak hands into strong hands, reinforcing the structural bid beneath the market. Meanwhile, gold miners are at a major technical inflection point. A 40-year resistance level has flipped into major support, nothing more technically bullish, according to Tavi Costa. Miners are also executing record levels of share buybacks, something never seen before at this scale, fuelled by exceptional profitability at current metal prices. This combination of improving fundamentals and depressed sentiment creates a compelling setup for patient investors.

This cooling interest is occurring against a building inflationary backdrop. Energy supply bottlenecks triggered by disruptions in the Strait of Hormuz are pushing up global energy costs, with flow restoration expected to take more than 60 days even if a peace agreement is reached. The resulting stickier inflation is keeping upward pressure on prices at a time when many investors have rotated aggressively into other themes, leaving gold temporarily out of favour.

Longer-term cycle view: Using 10-year rolling performance windows, monetary/hard assets like gold go through very long periods of out- and under-performance. We could be in the in the early innings of the current bull cycle for gold and related assets. Gold tends to move higher when investors are fearful of the future, and it tends to drag when investors are fearful of the present, as hiccups persist with the US-Iran conflict, Gold could trade lower, however, the inflation backdrop is difficult to ignore.

Emerging Markets: Taiwan Overtakes China — Concentration & Active Management

Taiwan has overtaken China as the biggest market in the MSCI Emerging Markets Index. Korea is on the rise too. However, these are highly concentrated indices. In MSCI Taiwan, TSMC comprises approximately 57% of the weight. In MSCI Korea, SK Hynix (~22%) and Samsung (~32%) together dominate. These three stocks alone account for 46% of the iShares Asia 50 ETF (IAA).

By comparison, even the S&P 500’s roughly 8% weighting in NVIDIA makes the US index look comically well-diversified. We know we are talking our own book, but this environment really highlights why active management is important to thoughtfully manage these concentrated exposures and identify the genuine beneficiaries within the AI and semiconductor supply chains.